Understanding Making Tax Digital terminology can feel overwhelming when HMRC introduces new digital requirements for sole traders and landlords. Many people confuse quarterly updates with final declarations, or wonder whether their spreadsheets meet digital record-keeping standards. This guide clarifies essential MTD terms and processes, helping you navigate the 2026 compliance requirements with confidence. By understanding the terminology, you'll avoid common mistakes and ensure smooth digital submissions throughout the tax year.

Table of Contents

- What Making Tax Digital (MTD) Means For Sole Traders And Landlords

- Key MTD Terms Every Sole Trader And Landlord Should Know

- How MTD Processes Work: From Record-Keeping To Software Submission

- Nuances And Important Considerations When Managing MTD Terminology And Compliance

- Explore VoxaMTD: Free Software Designed For Your MTD Needs

Key takeaways

| Point | Details |

|---|---|

| Quarterly digital updates required | You must submit income and expense summaries four times yearly using HMRC-approved software starting April 2026. |

| Qualifying income threshold matters | Self-employment and property income over £50,000 triggers MTD obligations, excluding capital gains and dividends. |

| Final declaration differs from updates | Annual final declaration includes all reliefs, adjustments, and additional income beyond quarterly submissions. |

| Compatible software is mandatory | Your software must meet HMRC minimum functionality standards and maintain digital links throughout. |

| Digital records reduce compliance errors | Electronic record-keeping through approved systems cuts the tax gap by addressing the £5 billion Self Assessment shortfall. |

What making tax digital (MTD) means for sole traders and landlords

Making Tax Digital represents HMRC's shift towards digital tax management, requiring you to maintain electronic records and submit information through approved software. Unlike traditional annual tax returns, MTD for ITSA aims to reduce errors and simplify tax compliance by breaking the process into manageable quarterly submissions.

The system applies specifically to Income Tax Self Assessment for sole traders and landlords whose qualifying income exceeds £50,000 annually. This threshold applies to gross income from self-employment and property rentals before deducting expenses. If your combined qualifying income reaches this level, you'll need to comply with MTD requirements from April 2026 onwards.

MTD fundamentally changes how you interact with HMRC throughout the tax year:

- You maintain digital records of all business income and expenses using compatible software

- You submit quarterly updates summarising your financial activity for each period

- You complete a final declaration at year end, similar to a traditional tax return but building on quarterly data

- Your software creates digital links between records and submissions, eliminating manual data transfer

The official MTD for ITSA guidance emphasises that this approach reduces calculation errors and gives you a clearer picture of your tax position throughout the year, rather than facing surprises at year end.

Pro Tip: Start exploring free MTD software now, even if your income currently sits below the threshold. Early adoption gives you time to familiarise yourself with digital processes before they become mandatory.

Key mtd terms every sole trader and landlord should know

Grasping MTD terminology helps you communicate effectively with HMRC, your accountant, and software providers. These definitions form the foundation of your compliance understanding.

Digital records refer to business information stored electronically in a format compatible with HMRC-approved software. Paper receipts converted to digital images don't automatically qualify unless your software processes them appropriately. Your records must capture all income sources, allowable expenses, and supporting documentation in a structured digital format that maintains audit trails.

Quarterly updates represent periodic submissions to HMRC covering your income and expenses for each three-month period. These updates provide snapshots of your business activity but exclude tax reliefs, adjustments, or final calculations. Think of them as progress reports rather than complete tax returns.

The final declaration serves as your comprehensive annual submission, replacing the traditional Self Assessment tax return. This declaration includes all income sources (even those outside MTD scope), claims for reliefs and allowances, pension contributions, and any adjustments to earlier quarterly updates. You submit this after your tax year ends, typically by 31 January.

Qualifying income determines whether MTD applies to you. This specifically means gross income from self-employment and property rentals before expenses. Capital gains, dividends, and employment income don't count towards the MTD threshold, though you still report them in your final declaration.

Compatible software meets HMRC's minimum functionality standards, enabling you to keep digital records, prepare quarterly updates, and submit information directly to HMRC systems. The software must maintain digital links throughout, preventing manual data copying between different systems.

Agent authorisation allows your accountant or tax agent to interact with HMRC on your behalf through MTD systems. You grant this permission digitally, enabling your agent to submit updates, view your tax position, and manage compliance requirements without requiring separate logins or paper authorisations.

Pro Tip: Create a simple glossary document with these terms and your personal notes about how each applies to your specific situation. This reference sheet becomes invaluable when discussing MTD with advisers or troubleshooting software issues.

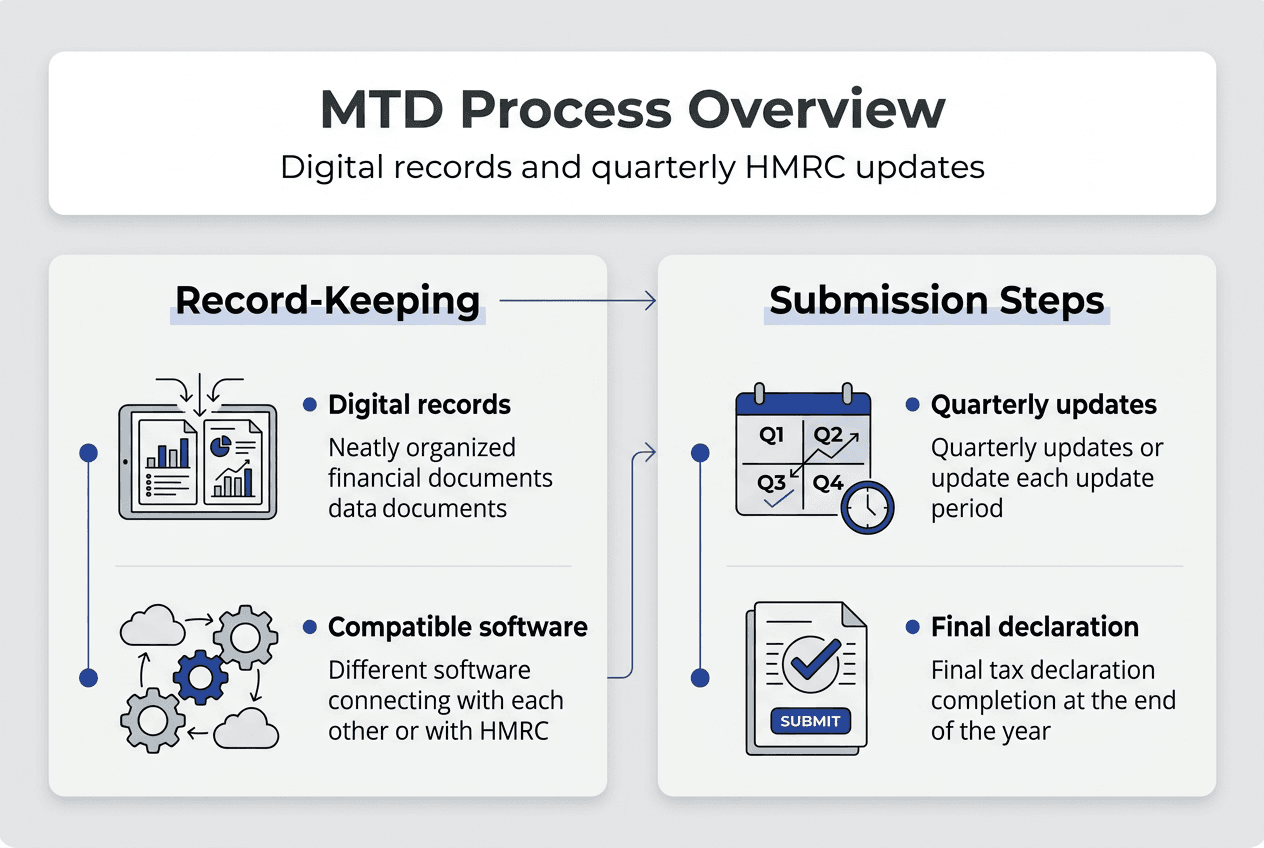

How mtd processes work: from record-keeping to software submission

From April 2026, self-employed people and landlords will need to keep digital tax records and send updates to HMRC four times a year. Understanding the practical workflow helps you prepare systems and routines that make compliance manageable.

Your digital record-keeping begins the moment MTD applies to you. Every business transaction, whether income received or expense paid, gets recorded in your compatible software. The software automatically categorises transactions, maintains running totals, and preserves the digital links HMRC requires. You can't manually type quarterly figures into HMRC systems; the data must flow digitally from your records.

The quarterly update cycle follows your accounting periods, typically aligned with standard tax quarters:

- 6 April to 5 July (due by 5 August)

- 6 July to 5 October (due by 5 November)

- 6 October to 5 January (due by 5 February)

- 6 January to 5 April (due by 5 May)

Each update summarises your total income and allowable expenses for that period. You don't calculate tax owed or claim reliefs at this stage. The updates simply inform HMRC of your business activity, allowing them to track your progress and flag potential issues early.

Compatible software can be a single product or a set of compatible products that work together through digital links. If you prefer spreadsheets for daily record-keeping, bridging software can connect your spreadsheet data to HMRC-approved submission software. The critical requirement is maintaining digital links without manual copying or retyping.

| Compliance step | Frequency | Key requirements | Deadline |

|---|---|---|---|

| Digital record-keeping | Ongoing | Capture all income and expenses electronically using compatible software | Daily or weekly |

| Quarterly updates | Four times yearly | Submit income and expense totals for each quarter via approved software | One month after quarter end |

| Final declaration | Annually | Complete comprehensive return including reliefs, adjustments, and all income | 31 January following tax year |

Pro Tip: Set calendar reminders two weeks before each quarterly deadline. This buffer gives you time to review records, correct errors, and submit updates without last-minute stress.

Explore MTD digital record-keeping software that automates transaction categorisation and deadline tracking, reducing your administrative burden significantly.

Nuances and important considerations when managing MTD terminology and compliance

Several subtle points about MTD terminology and requirements catch people by surprise. Understanding these nuances prevents compliance mistakes and unnecessary penalties.

Only specific income types count towards your MTD threshold. Self-employment profits and property rental income determine whether you exceed £50,000 and must comply. Excluded income, such as capital gains and dividend income, does not count toward the threshold for MTD compliance but must still be included in the Final Declaration. This distinction matters when you're close to the threshold or have multiple income streams.

Quarterly updates and final declarations serve different purposes, though people often confuse them:

| Aspect | Quarterly updates | Final declaration |

|---|---|---|

| Content | Income and expenses only | All income, reliefs, adjustments |

| Tax calculation | Not included | Complete tax calculation |

| Frequency | Four times yearly | Once annually |

| Deadline | One month after quarter | 31 January |

| Purpose | Progress reporting | Final tax assessment |

Joint property ownership requires careful attention to individual income calculations. If you own rental property with a partner, HMRC assesses your share of rental income individually. Your £25,000 share might not trigger MTD requirements alone, but your partner's additional self-employment income could push their total over the threshold, requiring them to comply whilst you remain outside MTD scope.

The tax gap for Self Assessment businesses is around 18.5%, or £5 billion, largely attributed to errors and incomplete record-keeping. MTD's digital links aim to close this gap by eliminating manual data transfer mistakes.

Common mistakes to avoid:

- Assuming any digital record qualifies (software must meet HMRC standards)

- Copying data manually between systems (breaks required digital links)

- Treating quarterly updates as complete tax returns (they're preliminary reports)

- Forgetting to include non-qualifying income in final declarations (everything gets reported eventually)

- Waiting until deadlines approach to review software compatibility (transition takes time)

Pro Tip: Review your current accounting software's MTD compatibility now. If it doesn't meet requirements, you'll need software for MTD compliance or bridging software to connect your existing tools to HMRC systems. Making this change mid-tax year creates unnecessary complications.

Understanding quarterly updates and final declaration differences helps you plan your compliance workflow and avoid submitting incomplete information at the wrong stage.

Explore VoxaMTD: free software designed for your MTD needs

Navigating MTD terminology becomes significantly easier when you use purpose-built software that handles the complexity for you. VoxaMTD offers free HMRC-approved software specifically designed for sole traders and landlords facing 2026 compliance requirements.

The platform automates digital record-keeping, categorises expenses through AI, and manages quarterly submission deadlines without manual intervention. You connect your bank accounts securely through open banking, allowing transactions to flow directly into your records whilst maintaining the digital links HMRC requires. The integrated accountant review service provides professional oversight before submissions, ensuring accuracy and giving you confidence in your compliance.

Whether you're just reaching the income threshold or have managed self-employment taxes for years, VoxaMTD free MTD software simplifies the transition to digital tax management. The platform guides you through each compliance step, translates MTD terminology into plain language, and tracks deadlines automatically. Explore the free version today to experience how purpose-built software transforms MTD compliance from overwhelming to manageable.

FAQ

What income counts towards making tax digital eligibility?

MTD for ITSA covers qualifying income from property and self-employment only. Capital gains, dividends, employment income, and savings interest don't count towards the £50,000 threshold, though you still report them in your final declaration. Calculate your gross self-employment and property income before expenses to determine MTD eligibility.

How do quarterly updates differ from the final declaration?

Quarterly updates require income and expense totals but exclude tax reliefs or adjustments initially; the final declaration is comprehensive. Think of quarterly updates as progress reports showing business activity, whilst the final declaration calculates your actual tax liability including all reliefs, pension contributions, and adjustments. You submit four quarterly updates throughout the year, then one final declaration after the tax year ends.

Can I use spreadsheets for MTD digital record-keeping?

Spreadsheets alone don't meet MTD requirements because they lack the digital links to HMRC systems. Bridging software is necessary to link spreadsheets with HMRC-approved software for MTD compliance. You can continue using spreadsheets for daily record-keeping, but you need bridging software to transfer data digitally to submission software without manual copying.

When do MTD requirements start for sole traders and landlords?

MTD for Income Tax Self Assessment begins in April 2026 for sole traders and landlords with qualifying income over £50,000. If your self-employment and property income combined exceeds this threshold, you must keep digital records and submit quarterly updates from the start of the 2026/27 tax year. HMRC may extend requirements to lower income thresholds in future years.

What happens if I miss a quarterly update deadline?

Missing quarterly deadlines can result in penalties, though HMRC typically applies these progressively based on how late your submission arrives. Initial penalties start small but increase for repeated or extended delays. More importantly, late updates prevent you from having an accurate view of your tax position throughout the year, potentially causing cash flow problems when your final liability becomes clear.