Managing quarterly submissions under Making Tax Digital can feel overwhelming, especially if you're juggling multiple income streams or clients. From April 2026, sole traders and landlords with qualifying income must submit digital quarterly summaries, marking a significant shift from traditional annual reporting. Errors, missed deadlines, and administrative burdens can quickly escalate costs and compliance risks. This guide breaks down preparation, execution, and verification steps to help you navigate MTD quarterly reporting with confidence and efficiency.

Table of Contents

- Key takeaways

- Understanding MTD quarterly reporting requirements

- Preparing for your MTD quarterly submissions

- Executing the MTD quarterly reporting process

- Common challenges and solutions for MTD quarterly reporting

- Streamline your MTD reporting with VoxaMTD

- Frequently asked questions about MTD quarterly reporting

Key Takeaways

| Point | Details |

|---|---|

| MTD quarterly required | From April 2026 sole traders and landlords with qualifying income must submit digital quarterly summaries via HMRC compatible software. |

| Digital records essential | Maintain accurate digital records of all income and expenses and submit via approved software connected to HMRC API. |

| Software chosen early | Select a compatible software solution promptly to avoid last minute pressure and ensure it supports both self employment and property income if needed. |

| Spreadsheets bridged option | If using spreadsheets, employ bridging software or migrate to dedicated MTD software for better automation and error checking. |

| Backlog prevention routines | Establish daily or weekly data entry to prevent quarterly backlogs and reduce errors. |

Understanding MTD quarterly reporting requirements

Making Tax Digital for Income Tax Self Assessment (MTD ITSA) fundamentally changes how sole traders and landlords report their income. If your gross income from self-employment or property exceeds £50,000 from the 2024/25 tax year onwards, you must submit four cumulative quarterly summaries digitally. This threshold drops to £30,000 in 2027 and £20,000 in 2028, expanding the number of affected businesses significantly.

Each tax year requires four quarterly updates, covering periods ending in July, October, January, and April. These submissions are cumulative, meaning each quarter includes all income and expenses from the start of the tax year to that quarter's end. After submitting all four updates, you must file an End of Period Statement (EOPS) and a Final Declaration by 31 January following the tax year.

Digital submission is mandatory. You cannot simply email spreadsheets to HMRC. If you currently use spreadsheets, you'll need bridging software to connect them to HMRC's systems. Free MTD software options exist specifically for sole traders and landlords, eliminating the need for expensive accounting packages.

Key requirements include:

- Maintaining digital records of all business and rental income and expenses

- Submitting quarterly summaries via HMRC-compatible software

- Filing an EOPS after each accounting period

- Completing a Final Declaration by 31 January after the tax year ends

- Ensuring all submissions use approved software that connects via HMRC's API

Understanding these requirements early allows you to choose appropriate software, organise your records, and avoid last-minute compliance scrambles. The transition from annual to quarterly reporting demands more frequent attention, but proper preparation makes the process manageable.

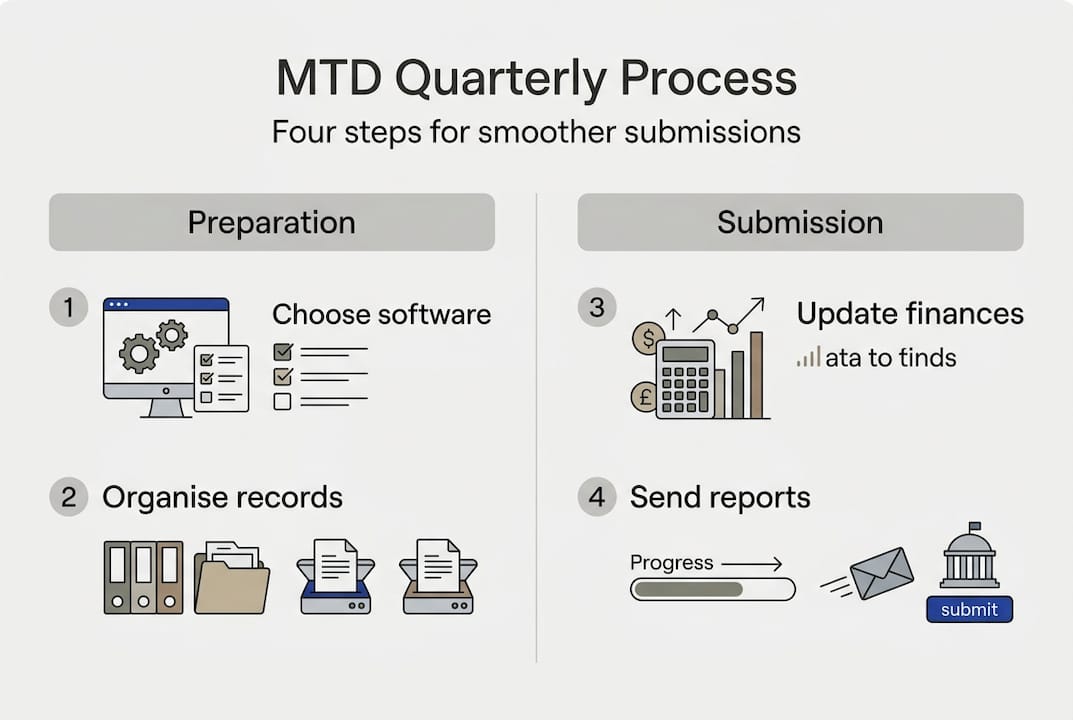

Preparing for your MTD quarterly submissions

Successful quarterly reporting starts long before your first submission deadline. Preparation involves selecting the right software, organising your records, and establishing routines that prevent quarterly backlogs.

Choose your MTD-compatible software as soon as possible. Waiting until the mandatory start date creates unnecessary pressure. Evaluate options based on your business structure, whether you need features for both self-employment and property income, and how well the software integrates with your existing workflows. Free MTD software designed for sole traders and landlords offers a cost-effective starting point without sacrificing compliance.

Digital record keeping forms the foundation of MTD reporting. Keep digital records in MTD-compatible software or bridging tools, categorising income and expenses to submit summaries via API to HMRC. This means recording every transaction with appropriate categories that align with your tax return boxes, such as SA103 for turnover or SA105 for property income.

If you currently use spreadsheets, you have two options: continue with bridging software that connects your spreadsheets to HMRC, or migrate to dedicated MTD software. Bridging tools work for simple businesses, but dedicated software often provides better automation, categorisation, and error checking.

Establish daily or weekly record-keeping habits rather than quarterly catch-ups. Entering transactions as they occur takes minutes, whilst quarterly backlogs can consume hours and increase error rates. Set reminders to review your records regularly, ensuring nothing falls through the cracks.

Organise your income and expenses according to tax return categories from the start. This alignment simplifies quarterly submissions and reduces the risk of miscategorisation. Review your previous year's tax return to identify which boxes apply to your business, then structure your digital records accordingly.

Pro Tip: Before your first quarterly submission, run a trial report covering a month or quarter to identify any categorisation issues or missing information whilst you still have time to correct them.

Executing the MTD quarterly reporting process

Once your records are organised and your software is configured, executing quarterly submissions becomes a straightforward routine. Understanding the cumulative nature of MTD reporting is crucial for accuracy and efficiency.

The four quarterly periods typically align with standard dates: 5 April to 5 July (Q1), 6 July to 5 October (Q2), 6 October to 5 January (Q3), and 6 January to 5 April (Q4). Your software will prompt you when each submission is due, usually within one month after the quarter ends.

Cumulative reporting allows error correction without formal amendments. If you discover a mistake in Q1 after submission, you simply include the correction in your Q2 figures. Since each quarterly summary reports all income and expenses from the tax year start to that quarter's end, subsequent submissions naturally override previous data.

Follow these steps for each quarterly submission:

- Review all transactions entered during the quarter for accuracy and completeness

- Verify that income and expenses are categorised correctly according to tax return boxes

- Check for any missing invoices, receipts, or bank transactions

- Run a preliminary report to identify any unusual figures or potential errors

- Submit the quarterly summary through your MTD software

- Save confirmation of submission and any reference numbers provided

After submitting all four quarterly updates, you must file an End of Period Statement. This finalises your accounting period and allows you to make any adjustments for items you deferred during quarterly reporting, such as capital allowances or complex expense allocations.

The Final Declaration, due by 31 January after the tax year ends, represents your formal submission equivalent to the old Self Assessment tax return. This is your last opportunity to ensure all figures are accurate before HMRC calculates your tax liability.

Comparison of reporting approaches:

| Feature | Traditional annual | MTD quarterly |

|---|---|---|

| Frequency | Once per year | Four times per year plus final declaration |

| Submission method | Paper or online form | Digital via compatible software only |

| Record keeping | Annual summary acceptable | Ongoing digital records mandatory |

| Error correction | Amendments after submission | Cumulative updates in subsequent quarters |

| Compliance burden | Concentrated annual effort | Distributed throughout year |

| Accuracy potential | Higher risk of forgotten items | Better accuracy through regular review |

Pro Tip: Set calendar reminders two weeks before each quarterly deadline to review your records and address any issues before the submission window closes.

Common challenges and solutions for MTD quarterly reporting

Transitioning to quarterly digital reporting presents several challenges, but understanding them in advance allows you to implement effective solutions.

Administrative burden increases significantly compared to annual reporting. Instead of one concentrated effort per year, you now face four quarterly submissions plus the EOPS and Final Declaration. This requires more frequent attention to bookkeeping and can feel overwhelming, especially for sole traders managing their own compliance.

Software compatibility and costs concern many businesses. ICAEW highlights admin burden, software availability issues, and underestimated costs as key challenges. Whilst some software options are free, others charge monthly or annual fees that add up quickly. Evaluate your needs carefully and consider starting with free MTD software before committing to paid solutions.

HMRC support and guidance, whilst improving, still leave some businesses uncertain about specific scenarios. Complex situations involving multiple income streams, partnerships, or unusual expenses may not be clearly addressed in official guidance. Seeking advice from an accountant or tax adviser can prevent costly mistakes.

Accountants play a vital role in mitigating MTD complexity. By automating expense categorisation and reviewing client income early in the process, they reduce errors and ensure compliance. If you work with an accountant, establish clear communication about who handles data entry, who reviews submissions, and when handoffs occur.

Key solutions to common challenges:

- Implement automation tools that categorise transactions based on rules you define

- Connect bank feeds to import transactions automatically, reducing manual entry

- Schedule regular bookkeeping sessions rather than quarterly marathons

- Use software with built-in compliance checks that flag potential errors

- Establish clear workflows with your accountant if you use professional support

"The transition to MTD quarterly reporting demands careful planning to balance compliance requirements with practical business operations. Early preparation and appropriate technology significantly reduce the administrative burden."

Cost management requires strategic thinking. Free software handles basic needs for many sole traders and landlords. If your business requires advanced features like inventory management or multi-currency support, paid options may justify their cost through time savings and error reduction.

Data security deserves attention when selecting software. Ensure your chosen platform uses encryption, secure authentication, and regular backups. HMRC-recognised software must meet specific security standards, providing baseline protection for your financial data.

Streamline your MTD reporting with VoxaMTD

Navigating quarterly submissions doesn't have to drain your time or budget. VoxaMTD offers free, HMRC-compliant software specifically designed for UK sole traders and landlords facing MTD requirements.

Our platform simplifies digital record keeping with intuitive categorisation, automated bank feeds, and built-in compliance checks that catch errors before submission. Whether you're managing self-employment income, rental properties, or both, VoxaMTD handles the complexity whilst you focus on running your business.

The integrated accountant review service allows professional oversight before each submission, combining the convenience of self-service software with expert verification. Set up takes minutes, and our reminder system ensures you never miss a quarterly deadline. Explore VoxaMTD's free MTD software to experience how straightforward quarterly reporting can be when you have the right tools supporting your compliance journey.

Frequently asked questions about MTD quarterly reporting

What is MTD quarterly reporting?

MTD quarterly reporting requires eligible sole traders and landlords to submit four cumulative digital summaries per tax year showing income and expenses, followed by an End of Period Statement and Final Declaration. This replaces the traditional annual Self Assessment for qualifying businesses.

Who needs to comply with MTD quarterly reporting?

Sole traders and landlords with gross income over £50,000 from the 2024/25 tax year onwards must comply from April 2026. The threshold drops to £30,000 in 2027 and £20,000 in 2028, progressively expanding the affected population.

What software options are available for MTD quarterly reporting?

You must use HMRC-compatible software or bridging tools that connect spreadsheets to HMRC systems. Free options like VoxaMTD provide full compliance for sole traders and landlords, whilst paid software offers additional features for complex businesses.

Can accountants help manage the MTD quarterly process?

Accountants can act as authorised agents, submitting quarterly updates on your behalf. They use automation tools for categorisation and conduct client reviews to improve accuracy, significantly reducing your compliance burden and error risk.

How do I correct mistakes in quarterly submissions?

The cumulative nature of quarterly reporting means subsequent submissions automatically update previous figures. If you find an error in Q1, include the correction in your Q2 submission. The Final Declaration provides a final opportunity to ensure complete accuracy before HMRC calculates your tax liability.