Many sole traders and landlords believe Making Tax Digital only affects VAT-registered businesses or that their annual Self Assessment tax returns will continue unchanged. This assumption can lead to unexpected compliance issues when HMRC's new quarterly reporting requirements take effect. MTD for Income Tax Self Assessment fundamentally changes how you report business income and property earnings, introducing digital record keeping and regular submissions that replace the traditional once-yearly approach. Understanding these regulations now helps you prepare your systems, choose compatible software, and avoid penalties when the rules apply to your income threshold.

Table of Contents

- Key takeaways

- What are MTD regulations and who must comply?

- How to comply with MTD regulations: record keeping and submissions

- Penalties and exemptions under the MTD regime

- Benefits and challenges of complying with MTD regulations

- How VoxaMTD can support your MTD compliance

- What are the common questions about MTD regulations?

Key Takeaways

| Point | Details |

|---|---|

| Digital records required | You must keep digital records including the date, amount and category for every transaction as part of MTD for Income Tax Self Assessment. |

| Thresholds and timing | The mandatory start is 6 April 2026 for gross income over £50,000, reducing to £30,000 from 2027 and £20,000 from 2028. |

| Quarterly submission deadlines | Quarterly updates must be submitted by 7 August, 7 November, 7 February and 7 May for each quarter. |

| Software compatibility and bridging solutions | Choose compatible software or an agent to ensure digital links between systems, with bridging solutions allowed during the initial implementation period. |

What are MTD regulations and who must comply?

Making Tax Digital represents HMRC's initiative to digitise tax administration for Income Tax Self Assessment, fundamentally changing how sole traders and landlords report their earnings. The system requires eligible taxpayers to maintain digital records and submit quarterly updates summarising their income and expenses, moving away from the traditional annual-only reporting model.

The regulations apply based on your combined gross income from self-employment and property sources. Mandatory from 6 April 2026 for those with gross income over £50,000, the threshold reduces to £30,000 from April 2027 and £20,000 from April 2028. This phased approach gradually brings more taxpayers into the MTD regime over three years.

Key groups affected by MTD include:

- Sole traders operating businesses with qualifying income levels

- Landlords receiving rental income from UK property

- Individuals with combined self-employment and property income above thresholds

- Those currently filing Self Assessment returns for business or property income

Partnerships and limited companies are not yet mandated under MTD for Income Tax Self Assessment, though this may change in future years. Certain exemptions apply for individuals experiencing digital exclusion due to age, disability, religious beliefs, or remote location. Trustees, executors, charities, and those without National Insurance numbers receive automatic exemptions from the requirements.

Choosing free MTD software for sole traders and landlords early allows you to familiarise yourself with digital record keeping before the mandatory start date. Testing systems during the voluntary period helps identify any technical issues or workflow adjustments needed for smooth quarterly reporting.

Pro Tip: Calculate your gross income now to determine which threshold year applies to you, giving you adequate preparation time before your compliance date arrives.

How to comply with MTD regulations: record keeping and submissions

Meeting MTD requirements involves maintaining digital records to specific standards and submitting quarterly updates according to HMRC's timeline. Your records must capture three essential elements for every business transaction: the date it occurred, the amount involved, and the appropriate category for that income or expense.

The digital links requirement means information must flow between software components without manual re-entry, though HMRC permits spreadsheets with bridging solutions during the initial implementation period. Digital records must include date, amount, category, with quarterly updates summarising your business activity for each three-month period.

Quarterly submission deadlines follow a consistent pattern:

- First quarter (6 April to 5 July): Submit by 7 August

- Second quarter (6 July to 5 October): Submit by 7 November

- Third quarter (6 October to 5 January): Submit by 7 February

- Fourth quarter (6 January to 5 April): Submit by 7 May

Each quarterly update provides HMRC with a summary of your income and expenses for that period, replacing the single annual submission under the old system. After completing all four quarterly updates, you submit an End of Period Statement confirming the information is complete and accurate. The Final Declaration, submitted by 31 January following the tax year end, replaces the traditional detailed Self Assessment tax return.

Agents can handle submissions on your behalf if you authorise them through HMRC's online services. This option suits taxpayers who prefer professional oversight of their compliance obligations or lack confidence managing digital submissions independently. Compatible MTD compliant software options streamline the entire process by automating calculations, tracking deadlines, and formatting data according to HMRC specifications.

Pro Tip: Start practising quarterly submissions during the voluntary period to identify any record keeping gaps or software issues before mandatory compliance begins, reducing stress when deadlines become enforceable.

Penalties and exemptions under the MTD regime

Understanding the penalty structure helps you prioritise compliance and avoid unnecessary fines. HMRC applies different penalty types depending on whether issues involve late submissions, late payments, inaccuracies, or inadequate record keeping.

The points-based penalties for late submissions accumulate when you miss quarterly update deadlines. You receive one point for each late submission, with a £200 fixed penalty triggered after reaching the four-point threshold. Additional points beyond four result in further £200 penalties for each subsequent late submission. Points expire after 24 months of compliant behaviour, allowing you to reset your record through consistent on-time filing.

Late payment penalties follow a separate structure:

- First late payment: penalty equals 5% of unpaid tax

- Payment still outstanding after 30 days: additional 5% penalty

- Payment still outstanding after 6 months: further 5% penalty

- Payment still outstanding after 12 months: final 5% penalty

Inaccuracy penalties depend on the behaviour causing the error, ranging from no penalty for reasonable care taken, up to 100% of tax lost for deliberate and concealed inaccuracies. Poor record keeping that prevents accurate tax calculations can also attract penalties, emphasising the importance of maintaining complete digital records throughout each tax year.

The soft landing period for 2026/27 means HMRC will not apply penalty points for late quarterly submissions during the first year of mandatory compliance, giving taxpayers time to adjust to the new system without immediate financial consequences.

Exemptions from MTD requirements apply in specific circumstances. Digital exclusion grounds include age (if you are too old to use digital tools), disability (if conditions prevent digital engagement), religious beliefs (if they prohibit computer use), or remote location (if you lack internet access). You must apply for these exemptions and provide supporting evidence demonstrating why digital compliance is not reasonably practicable for your situation.

Automatic exemptions apply to trustees managing estates, executors handling deceased persons' tax affairs, charities registered with HMRC, and individuals without National Insurance numbers. These groups continue using traditional paper-based reporting methods until HMRC extends MTD requirements to their circumstances.

Pro Tip: Set calendar reminders for submission deadlines at least one week before the due date, allowing time to resolve any technical issues or data queries without risking penalty points.

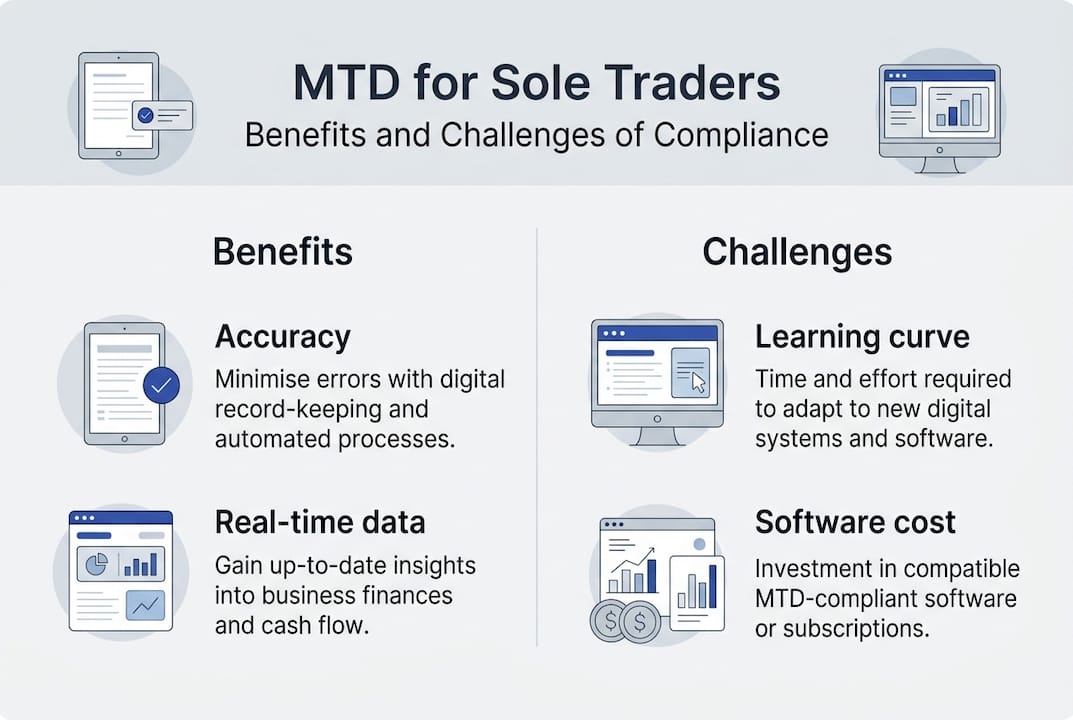

Benefits and challenges of complying with MTD regulations

MTD compliance brings tangible advantages alongside practical hurdles that taxpayers must navigate. Understanding both sides helps you prepare realistic expectations and plan your transition strategy effectively.

Digital record keeping improves accuracy by reducing manual data entry errors and providing real-time visibility of your business finances. Quarterly updates spread the reporting workload across the year rather than concentrating everything into a single annual deadline, potentially reducing stress and last-minute scrambling. MTD VAT experience showed increased record accuracy and significant time savings through automation, though costs and benefits varied among different user types.

| Aspect | Benefits | Challenges |

|---|---|---|

| Record keeping | Digital systems reduce errors, provide real-time financial visibility | Learning new software, maintaining digital discipline throughout year |

| Submissions | Quarterly updates spread workload, reduce year-end pressure | Four deadlines instead of one, requires consistent engagement |

| Costs | Free software options available, potential time savings | Premium features may require payment, initial setup time investment |

| Support | Agent services available, HMRC guidance resources | Finding reliable advice, understanding technical requirements |

| Compliance | Clear digital audit trail, automated calculations | Adapting workflows, ensuring digital links meet requirements |

Challenges include the cost of implementing new software, particularly for taxpayers who previously managed records using basic spreadsheets or paper systems. Learning digital record keeping requires time investment, especially for individuals less comfortable with technology. Managing four quarterly deadlines demands more consistent engagement with your bookkeeping throughout the year compared to the traditional annual approach.

Steps to ease your MTD transition:

- Research and test free MTD software solutions well before your mandatory compliance date

- Attend training sessions or webinars offered by software providers and professional bodies

- Review your current record keeping system and identify gaps that need addressing

- Consider engaging an accountant or tax agent if you lack confidence managing digital submissions

- Start voluntary quarterly reporting before mandatory compliance begins to build familiarity

- Set up automated bank feeds and receipt capture tools to minimise manual data entry

The transition period offers opportunities to streamline your business administration beyond just tax compliance. Many taxpayers discover that regular quarterly reviews help them spot financial trends earlier, make better business decisions, and maintain closer control over their cash flow throughout the year.

How VoxaMTD can support your MTD compliance

Navigating MTD regulations becomes significantly easier with purpose-built software designed specifically for UK sole traders and landlords. VoxaMTD simplifies quarterly submissions by automating digital record keeping, tracking deadlines, and formatting data according to HMRC specifications without requiring technical expertise.

The platform supports both self-employment income and property earnings within a single system, eliminating the need for separate tools or manual consolidation. Integrated features include automatic categorisation of expenses, secure bank connections through open banking, and submission reminders that help you avoid penalty points. Agent access functionality allows your accountant to review records and handle submissions on your behalf, combining professional oversight with user-friendly self-service capabilities.

Key features that streamline your compliance:

- Automatic digital links between record keeping and submission functions

- Deadline tracking with email and SMS reminders for quarterly updates

- Agent access portal for professional review before filing

- Bank-grade encryption protecting your financial data

- Mobile app for capturing receipts and recording expenses on the go

Trying VoxaMTD free MTD software early allows you to integrate it smoothly into your bookkeeping routine, identifying any workflow adjustments needed before mandatory deadlines arrive. The platform's intuitive interface requires minimal training, helping you focus on running your business rather than wrestling with compliance technicalities.

Pro Tip: Set up your VoxaMTD account during the voluntary period to practise quarterly submissions without pressure, building confidence and familiarity before your compliance becomes mandatory.

What are the common questions about MTD regulations?

What deadlines apply for quarterly submissions?

Quarterly updates are due one month and two days after each quarter ends: 7 August, 7 November, 7 February, and 7 May. The End of Period Statement is due by 31 January following the tax year, with the Final Declaration also due by 31 January.

Can I use spreadsheets for MTD record keeping?

Yes, you can use spreadsheets during the initial implementation period if you employ bridging software to create digital links for submissions. However, the spreadsheet itself must capture date, amount, and category for all transactions, and manual copying between systems is not permitted.

Who can apply for exemptions from MTD?

You can apply for exemption if you experience digital exclusion due to age, disability, religious beliefs, or remote location without internet access. Trustees, executors, charities, and individuals without National Insurance numbers receive automatic exemptions without needing to apply.

How does MTD impact accountants working with clients?

Accountants can access client records through agent authorisation, reviewing quarterly submissions before filing and providing professional oversight throughout the year. This creates opportunities for more regular client engagement and proactive tax planning rather than annual-only interactions.

Are payment dates changing under MTD?

No, payment dates remain unchanged. You still pay balancing payments by 31 January following the tax year and payments on account by 31 January and 31 July. MTD only changes reporting frequency, not when tax payments are due.