Nearly 60% of UK sole traders and landlords remain unaware of the phased Making Tax Digital (MTD) deadlines rolling out from April 2026, creating significant compliance risks for businesses unprepared for quarterly digital reporting. Understanding these deadlines is essential to avoid penalties, maintain HMRC compliance, and adapt your bookkeeping systems before mandatory submission dates arrive. This guide clarifies the phased rollout timeline, quarterly update requirements, penalty structures, and practical preparation steps to help you navigate MTD income tax obligations with confidence.

Table of Contents

- Key takeaways

- Phased digital tax deadlines under Making Tax Digital

- Quarterly updates and final declaration deadlines explained

- Penalties and compliance tips for meeting digital deadlines

- How to prepare and stay compliant with digital tax deadlines

- Manage your digital tax deadlines with VoxaMTD software

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Phased rollout timeline | MTD begins on 6 April 2026 with thresholds starting at fifty thousand pounds and reducing each year to widen coverage. |

| Quarterly update deadlines | Submissions are due roughly one month after each quarter ends with four interim updates and the final declaration by 31 January. |

| Software sign up | Access to MTD is only via compatible software and cannot be registered directly with HMRC, which gives time to migrate data and test processes. |

| Record keeping and nil returns | Digital record keeping is required including nil returns and linking data across systems to meet MTD obligations. |

| Penalties and leniency | Penalties are calculated on a points basis but the first year offers leniency to ease transition. |

Phased digital tax deadlines under Making Tax Digital

The phased rollout from 6 April 2026 for qualifying income thresholds starting at £50,000 and reducing annually creates distinct compliance timelines for different income brackets. Understanding which threshold applies to your situation determines when you must begin digital quarterly reporting. This phased approach gives businesses time to adapt, but confusion about eligibility remains widespread.

The income thresholds operate on gross income before expenses from self-employment or property rental combined. If you earned £52,000 in gross trading income during the 2024-25 tax year, you fall into the first compliance wave starting 6 April 2026. The threshold drops to £30,000 for the 2027 rollout and £20,000 for 2028, eventually capturing most sole traders and landlords within the MTD framework.

HMRC sends notification letters to qualifying taxpayers, but relying solely on these notifications creates risk. System delays, address changes, or administrative errors can mean you miss crucial preparation time. Self-checking your gross income against the published thresholds ensures you know your obligations well before deadlines arrive. The MTD digital tax deadlines guide provides detailed threshold calculations and examples.

Pro Tip: Calculate your qualifying income by adding all self-employment and property rental gross income before any expense deductions, including income from multiple sources or properties.

Key preparation steps include:

- Verify your gross income against the applicable threshold for your tax year

- Identify which compliance wave applies to your business based on 2024-25, 2025-26, or 2026-27 income

- Register through free MTD software for sole traders rather than attempting direct HMRC signup

- Set up digital record-keeping systems at least three months before your compliance start date

- Review your current bookkeeping processes to identify gaps in digital linking requirements

| Tax year | Income threshold | Compliance start date | Affected taxpayers |

|---|---|---|---|

| 2024-25 | £50,000+ | 6 April 2026 | Approximately 1.2 million |

| 2025-26 | £30,000+ | 6 April 2027 | Additional 1.5 million |

| 2026-27 | £20,000+ | 6 April 2028 | Additional 1.8 million |

Software signup represents the only compliant pathway into MTD. HMRC does not offer direct website registration for MTD income tax, deliberately channelling all users through compatible software providers. This ensures digital record-keeping standards meet regulatory requirements from the outset. Choosing software early allows time to migrate historical data, test quarterly submission workflows, and train yourself or staff before mandatory deadlines begin.

Quarterly updates and final declaration deadlines explained

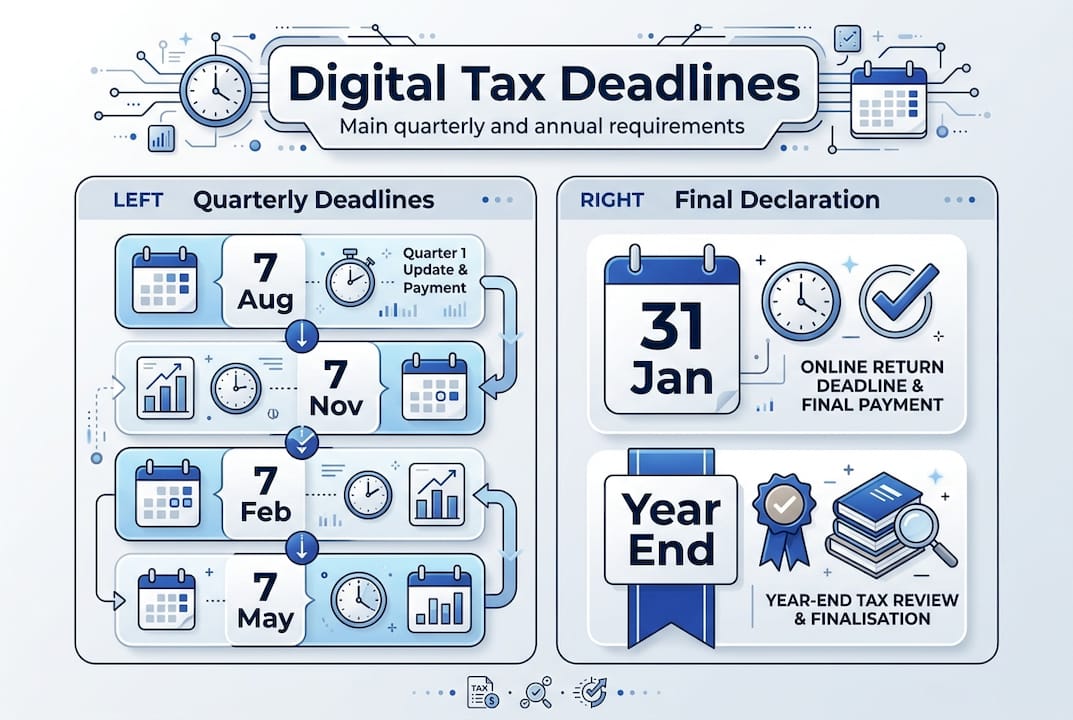

Quarterly update deadlines follow a consistent pattern throughout each tax year, with submissions due approximately one month after each quarter ends. The quarterly updates due about one month after quarter ends; final declaration by 31 January following tax year structure creates four interim reporting points plus one annual reconciliation. Understanding these dates prevents rushed submissions and compliance gaps.

The four quarterly deadlines fall on 7 August, 7 November, 7 February, and 7 May each year. Each update covers income and expenses for the preceding three-month period. For example, your 7 August submission reports activity from 6 April to 5 July. These updates do not calculate tax owed but instead provide HMRC with regular income and expense data throughout the year.

Final declarations serve a different purpose than quarterly updates. Submitted by 31 January following the tax year end, the final declaration reconciles all four quarterly updates, applies reliefs and allowances, and calculates your actual tax liability. This replaces the traditional self-assessment tax return for MTD participants. Payment deadlines remain unchanged at 31 January for the balancing payment and 31 July for the second payment on account.

Nil returns require submission even when you have no trading or rental activity during a quarter. Many sole traders and landlords mistakenly believe they can skip quarterly updates for inactive periods. MTD rules mandate digital submission of nil returns to maintain compliance status. Failing to submit nil returns triggers the same penalty points as missing updates with activity.

Pro Tip: Schedule quarterly update submissions for the first week after each deadline rather than waiting until the 7th to avoid last-minute technical issues or forgotten deadlines.

Quarterly submission workflow:

- Close your books for the quarter ending 5 July, 5 October, 5 January, or 5 April

- Review income and expense categorisation within your accounting software for MTD for accuracy

- Generate the quarterly update summary showing total income and allowable expenses

- Submit digitally to HMRC through your software before the 7th of the following month

- Retain confirmation of submission and any reference numbers provided

- Begin recording transactions for the next quarter immediately

| Quarter period | Quarter end date | Submission deadline | Content covered |

|---|---|---|---|

| Q1 | 5 July | 7 August | Income and expenses 6 April to 5 July |

| Q2 | 5 October | 7 November | Income and expenses 6 July to 5 October |

| Q3 | 5 January | 7 February | Income and expenses 6 October to 5 January |

| Q4 | 5 April | 7 May | Income and expenses 6 January to 5 April |

| Final declaration | 5 April | 31 January (following year) | Reconciliation of all quarters plus reliefs |

The MTD deadlines explained resource provides additional examples and edge case scenarios. Understanding the distinction between quarterly updates and final declarations prevents confusion about when tax calculations occur versus when you simply report activity.

Penalties and compliance tips for meeting digital deadlines

The points-based penalties start after accumulating 4 points with fines of £200+, with no penalties for late quarterly updates in the first year structure represents a significant shift from traditional fixed penalty amounts. Each late quarterly update adds one penalty point to your record. Once you accumulate four points, HMRC issues a £200 fine. Additional late submissions after reaching four points trigger further £200 penalties per occurrence.

Penalty points expire after 24 months of compliant submissions. If you submit all quarterly updates on time for two full years, your penalty point total resets to zero. This rolling window encourages consistent compliance rather than punishing past mistakes indefinitely. However, the cumulative nature means sporadic lateness quickly compounds into financial penalties.

The first compliance year offers crucial breathing room. For taxpayers entering MTD in April 2026, no penalty points accrue for late quarterly updates during the 2026-27 tax year. This grace period acknowledges the learning curve associated with new digital reporting requirements. HMRC still expects submissions but provides latitude for adjustment without immediate financial consequences.

"The first year penalty relief applies only to quarterly updates. Final declaration deadlines and payment dates maintain full penalty structures from day one, so late January submissions still incur standard self-assessment penalties."

Final declaration penalties follow existing self-assessment rules. Late submission after 31 January triggers an immediate £100 penalty, with additional daily penalties of £10 per day after three months (capped at £900). Six months late incurs a further penalty of 5% of tax owed or £300, whichever is greater. Twelve months late doubles this penalty. Payment penalties accrue separately at 5% of unpaid tax at 30 days, six months, and twelve months overdue.

Practical compliance strategies:

- Set calendar reminders two weeks before each quarterly deadline to allow review time

- Schedule a specific day each quarter for closing books and preparing submissions

- Use avoid MTD penalties software with built-in deadline alerts and submission tracking

- Maintain a compliance checklist covering digital linking, nil returns, and record retention

- Review submission confirmations immediately to catch any rejection or error messages

- Keep backup documentation of all digital submissions and HMRC correspondence

Digital linking failures represent a less obvious compliance risk. MTD requires digital transfer of data between software systems without manual re-entry. Copying figures from spreadsheets into submission software violates digital linking rules, potentially triggering compliance issues even if submissions occur on time. Ensuring your entire workflow maintains digital connectivity protects against this technical non-compliance.

Ignoring nil return requirements creates unnecessary penalty exposure. The MTD penalties guide emphasises that many first-year penalties stem from sole traders assuming they need not report inactive quarters. Treating every quarter as mandatory regardless of activity level eliminates this risk entirely.

How to prepare and stay compliant with digital tax deadlines

Registration through HMRC-compatible software represents the mandatory first step for MTD compliance. The sign up via compatible software, keep digital links between records, and submit mandatory nil returns if no activity in a quarter requirement means you cannot complete MTD signup directly on HMRC's website. This deliberate design ensures all participants use software meeting digital record-keeping and submission standards.

Digital linking requirements extend beyond simple data entry. Your entire bookkeeping workflow must maintain digital connectivity from transaction recording through final submission. Using spreadsheets to track income and expenses, then manually typing totals into submission software, fails MTD standards. Compliant systems digitally transfer data between record-keeping and submission functions without human re-entry.

Self-checking income thresholds annually protects against missed notifications. HMRC notification systems experience delays, address mismatches, and processing backlogs. Calculating your own qualifying income each tax year ensures you know your compliance obligations regardless of whether official notification arrives. This proactive approach prevents last-minute scrambles when deadlines approach.

Pro Tip: Review your gross income calculation in January each year, giving yourself three months to register and prepare systems before the April compliance start date if you cross the threshold.

Payment dates remain unchanged under MTD. The 31 January balancing payment and 31 July payment on account deadlines continue exactly as they operated under traditional self-assessment. MTD changes reporting frequency and methods but does not alter when you pay tax owed. Keeping these payment obligations separate from quarterly update deadlines prevents confusion about when money must reach HMRC.

Compliance preparation checklist:

- Register with MTD sign-up and software at least three months before your compliance start date

- Verify all software components maintain digital linking without manual data re-entry

- Set up bank feeds or import processes to capture all business transactions digitally

- Create a quarterly submission calendar with reminders two weeks before each deadline

- Establish a nil return submission process for quarters without trading activity

- Document your digital record-keeping workflow to demonstrate compliance if questioned

- Test your first quarterly submission well before the deadline to identify technical issues

| Compliance element | Requirement | Common mistake | Solution |

|---|---|---|---|

| Software signup | Must use HMRC-compatible software | Attempting direct HMRC website registration | Choose recognised software provider early |

| Digital linking | Data transfers digitally between systems | Manual re-entry of spreadsheet totals | Use integrated software with digital connectivity |

| Nil returns | Submit even with no activity | Skipping quarters without income | Treat every quarter as mandatory submission |

| Threshold checking | Self-verify gross income annually | Relying only on HMRC notifications | Calculate qualifying income each January |

| Payment timing | 31 January and 31 July unchanged | Confusing update deadlines with payment dates | Keep payment calendar separate from reporting |

The MTD compliance dates official resource provides detailed guidance on each compliance element. Planning reduces administrative burden significantly. Sole traders and landlords who establish systematic quarterly processes report spending 30-40% less time on tax compliance than those handling submissions reactively at each deadline.

Software selection impacts long-term compliance ease. Features like automated bank transaction imports, AI-powered expense categorisation, and built-in deadline reminders reduce manual work and error risk. Evaluating software capabilities before committing ensures your chosen system supports efficient compliance throughout the year, not just at submission deadlines.

Manage your digital tax deadlines with VoxaMTD software

Navigating MTD compliance becomes significantly simpler with purpose-built software designed specifically for UK sole traders and landlords. VoxaMTD free MTD software provides HMRC-recognised tools that handle digital record-keeping, quarterly update management, and deadline tracking in one integrated platform. The system maintains digital linking throughout your workflow, automatically categorises expenses using AI, and connects securely to your bank accounts through open banking.

The platform eliminates common compliance pitfalls through automated reminders and validation checks before submission. You receive alerts two weeks before each quarterly deadline, ensuring adequate preparation time. Built-in compliance verification confirms your records meet digital linking requirements and flags missing nil returns before they trigger penalties. MTD compliance tools include professional accountant review options, providing expert oversight before final submissions reach HMRC. This combination of automation and professional support helps sole traders and landlords maintain consistent compliance without becoming tax experts themselves.

Frequently asked questions

What are the digital tax deadlines under Making Tax Digital?

MTD introduces quarterly update deadlines on 7 August, 7 November, 7 February, and 7 May each year, with a final declaration due by 31 January following the tax year end. The phased rollout begins 6 April 2026 for those with income over £50,000, expanding to lower thresholds in subsequent years. Sole traders and landlords must submit digital updates for each quarter regardless of activity levels.

Who must comply with MTD income tax requirements?

Sole traders and landlords with qualifying income above the threshold for their tax year must comply. Qualifying income includes gross self-employment and property rental income before expenses. The threshold starts at £50,000 for 2024-25, reducing to £30,000 for 2025-26 and £20,000 for 2026-27. You should self-check your income annually rather than relying solely on HMRC notifications.

How do quarterly update deadlines and final declaration dates work?

Quarterly updates report income and expenses for three-month periods ending 5 July, 5 October, 5 January, and 5 April, with submissions due by the 7th of the following month. The final declaration reconciles all quarterly updates and calculates actual tax liability, due by 31 January after the tax year ends. Quarterly updates provide regular reporting, while the final declaration determines what you owe.

What happens if I miss a digital tax deadline?

Missing quarterly updates adds penalty points to your record, with £200 fines triggered after accumulating four points. Each subsequent late submission after reaching four points incurs additional £200 penalties. However, the first compliance year (2026-27) offers no penalty points for late quarterly updates, providing adjustment time. Final declaration penalties follow traditional self-assessment rules with immediate £100 fines for late submission.

How can I prepare to meet my digital tax deadlines?

Register through MTD-compatible software at least three months before your compliance start date, as direct HMRC website signup is not available. Ensure your entire record-keeping workflow maintains digital linking without manual data re-entry between systems. Submit nil returns for quarters without trading or rental activity to maintain compliance status. Verify your income against thresholds annually and set calendar reminders two weeks before each quarterly deadline to allow adequate preparation time.