Many UK sole traders and landlords believe tax digitisation only affects VAT-registered businesses or remains optional. That misconception ends in April 2026, when Making Tax Digital for Income Tax Self Assessment becomes mandatory for thousands of self-employed individuals and property owners. This guide explains the new quarterly reporting requirements, software obligations, and practical steps to ensure compliance while simplifying your tax administration.

Table of Contents

- Key takeaways

- What is UK tax digitisation and MTD for ITSA?

- How does the quarterly updating process work?

- Choosing the right software and staying compliant

- Why tax digitisation matters: reducing errors and the tax gap

- Simplify your MTD journey with VoxaMTD

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Software mandatory | You must store income and expense information in HMRC compatible software that can communicate directly with HMRC servers. |

| Quarterly updates replace annual returns | Updates are submitted four times a year instead of one annual tax return. |

| Threshold phased rollout | From April 2026 sole traders and landlords with annual income above £50,000 must comply, with the threshold reducing to £30,000 in 2027 and £20,000 in 2028. |

| Deadlines and penalties | Quarterly updates are due within one month of quarter end on dates such as 7 August, 7 November, 7 February and 7 May, and penalties may apply for late submissions. |

What is UK tax digitisation and MTD for ITSA?

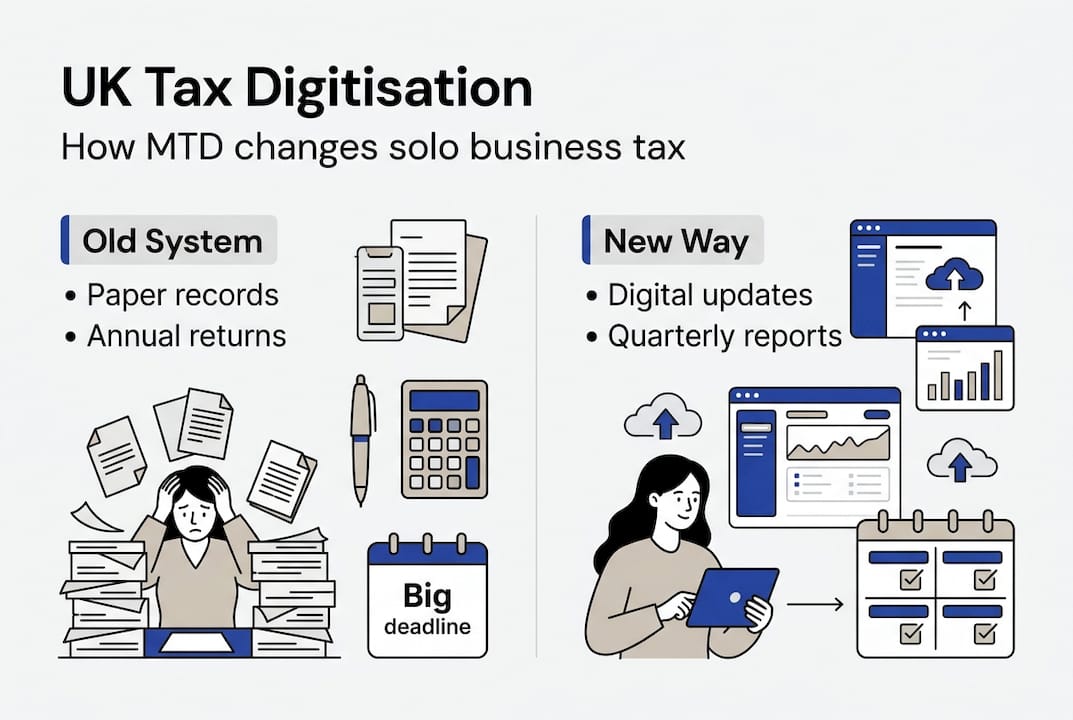

UK tax digitisation refers to Making Tax Digital for Income Tax Self Assessment, a HMRC programme requiring sole traders and landlords to keep digital records and submit quarterly updates. This initiative transforms how self-employed individuals and property owners report income and expenses, moving away from paper-based annual returns towards continuous digital engagement with HMRC throughout the tax year.

The rollout follows a phased approach based on income thresholds. From April 2026, sole traders and landlords with annual business or property income exceeding £50,000 must comply. This threshold drops to £30,000 in April 2027, then £20,000 in April 2028. These thresholds apply to gross income before expenses, meaning many more taxpayers will eventually fall within scope than initially anticipated.

Digital record-keeping replaces traditional paper ledgers and spreadsheets maintained outside HMRC systems. You must store income and expense information in HMRC-compatible software that can communicate directly with HMRC servers. This requirement ensures data accuracy and enables real-time visibility of your tax position.

Quarterly reporting introduces a fundamental shift from annual self-assessment. Instead of submitting one tax return covering the entire year, you provide updates four times annually. Each update summarises your income and expenses for the quarter, giving HMRC ongoing insight into your financial activity. This approach mirrors the existing MTD for VAT system that many businesses already use.

The programme applies specifically to income tax obligations, covering trading income from self-employment and property income from residential or commercial lettings. If you operate as a sole trader, freelancer, or landlord, MTD for ITSA likely affects you. Partnerships will also need to comply, with each partner maintaining digital records and submitting updates.

Who must comply:

- Sole traders with business income above the threshold

- Landlords with property income above the threshold

- Mixed income individuals combining employment and self-employment

- Portfolio landlords managing multiple properties

- Freelancers and contractors operating outside IR35

Using free MTD software simplifies the transition by automating record-keeping and submission processes. The right tools transform compliance from a burden into a manageable routine that actually improves your financial visibility.

How does the quarterly updating process work?

The quarterly updating process centres on cumulative reporting throughout the tax year, with each update building on previous submissions. Understanding this cycle helps you maintain compliance and avoid last-minute scrambles before deadlines.

The quarterly cycle follows these steps:

- Maintain digital records of all income and expenses using compatible software throughout the quarter

- Summarise your financial data at quarter end, categorising income sources and expense types

- Submit your quarterly update through the software within one month of quarter end

- Review the cumulative position shown by HMRC, which combines all updates to date

- Make any necessary adjustments in subsequent updates if you discover errors

Quarterly updates are cumulative summaries submitted within one month of quarter end with deadlines on 7 August, 7 November, 7 February, and 7 May. These dates apply regardless of your accounting period, creating a standardised reporting calendar for all taxpayers. Missing a deadline triggers penalties, so calendar reminders prove essential.

Each update requires specific data categories. You report total income received during the quarter, broken down by source such as trading income, property rental income, or other business income. Expenses follow similar categorisation, with HMRC expecting you to allocate costs to appropriate headings like premises costs, travel, professional fees, or financial charges.

| Quarter | Period covered | Submission deadline |

|---|---|---|

| Q1 | 6 April to 5 July | 7 August |

| Q2 | 6 July to 5 October | 7 November |

| Q3 | 6 October to 5 January | 7 February |

| Q4 | 6 January to 5 April | 7 May |

Quarterly updates differ fundamentally from your final declaration. Updates provide provisional figures that may change as you gather more information or correct mistakes. The final declaration, due by 31 January following the tax year end, crystallises your tax liability. At this stage, you confirm all figures, claim any additional reliefs or allowances, and calculate the final tax due.

Corrections follow a carry-forward approach. If you discover an error in a previous quarter, you simply adjust the figures in your next update rather than amending the original submission. The cumulative nature of the system means corrections automatically flow through to your year-to-date position. This flexibility reduces administrative burden compared to formal amendment procedures.

Pro tip: Set up automatic bank feeds in your MTD update software to capture transactions as they occur. This continuous approach eliminates quarter-end data entry marathons and ensures nothing gets forgotten when deadlines approach.

The MTD process also enables real-time tax estimates. After each quarterly update, HMRC calculates your projected annual tax liability based on current figures. This visibility helps you budget for tax payments and avoid surprises when the final bill arrives in January.

Choosing the right software and staying compliant

Selecting appropriate software forms the foundation of MTD compliance. HMRC maintains a list of compatible products, but not all solutions suit every business type or budget. Your choice should balance functionality, cost, and ease of use whilst ensuring full regulatory compliance.

Software must be HMRC-compatible, meaning it can connect directly to HMRC systems and submit updates in the required format. Bridging software provides an alternative for those preferring spreadsheets, acting as a conduit between your Excel records and HMRC servers. This option suits individuals comfortable with spreadsheet management but requires manual data transfer from spreadsheet to bridging tool.

Agents can submit updates on your behalf with proper authorisation. If you work with an accountant, they can manage your MTD obligations using their own software whilst you maintain digital records. This arrangement works well for complex tax situations or individuals who prefer professional oversight, though it typically incurs additional fees.

Software options include:

- Free MTD platforms offering basic income and expense tracking

- Paid subscriptions with advanced features like invoicing and inventory management

- Bridging software for spreadsheet users

- Accountancy practice software for agent submissions

- Industry-specific solutions tailored to property or freelance sectors

Typical software costs range from free for basic compliance tools to £10-30 monthly for feature-rich platforms. Free options provide sufficient functionality for straightforward sole trader or landlord scenarios. Premium tiers add capabilities like multi-currency support, project tracking, or CIS deductions that benefit specific business types.

Pro tip: Test MTD-compatible software options during a free trial period before committing. Ensure the interface feels intuitive and the categorisation logic matches your business activities to avoid frustration during actual use.

Continuous compliance requires several ongoing practices. Maintain regular data entry habits rather than quarterly catch-ups, as frequent small updates prove less overwhelming than quarterly marathons. Set calendar alerts for submission deadlines with buffer time for unexpected issues. Reconcile bank statements monthly to catch discrepancies early. Back up your digital records regularly, as HMRC expects you to retain information for at least five years.

Penalties apply for late submissions, starting at £200 for missing a quarterly deadline. Persistent non-compliance triggers daily penalties of £10 after 90 days, potentially reaching thousands of pounds annually. These consequences make reliable software and systematic processes essential investments rather than optional conveniences.

Security considerations matter when choosing software. Verify that platforms use encryption for data transmission and storage. Check whether the provider complies with UK data protection regulations. Understand where your financial information resides and who can access it. Reputable HMRC software providers publish clear privacy policies and security certifications.

Why tax digitisation matters: reducing errors and the tax gap

Beyond compliance obligations, tax digitisation delivers tangible benefits for both taxpayers and the wider economy. Understanding these advantages helps frame MTD as an opportunity rather than merely a regulatory burden.

Making Tax Digital aims to reduce the UK tax gap, estimated at 4.8-5.3%, by improving accuracy and compliance especially for self-assessment taxpayers including landlords. The tax gap represents the difference between tax theoretically owed and amounts actually collected. Self-assessment errors and omissions contribute significantly to this shortfall, with mistakes ranging from simple arithmetic errors to forgotten income sources.

Digital quarterly reporting catches errors earlier than annual submissions. When you update HMRC quarterly, discrepancies become apparent within weeks rather than months. This immediacy enables prompt corrections before figures become entrenched in your records. Earlier detection reduces the likelihood of cascading errors that compound throughout the year.

"Digital record-keeping eliminates transcription mistakes that plague paper-based systems. Automated bank feeds capture every transaction without manual data entry, whilst software validation rules flag unusual entries or missing information before submission."

Comparison between traditional and digital approaches illustrates the transformation:

| Aspect | Pre-MTD approach | Post-MTD approach |

|---|---|---|

| Record-keeping | Paper receipts, manual ledgers | Digital capture, automated categorisation |

| Error detection | Annual review, often too late | Quarterly validation, immediate correction |

| Tax planning | Reactive, based on year-end figures | Proactive, informed by quarterly estimates |

| HMRC interaction | Annual submission, infrequent contact | Quarterly updates, ongoing dialogue |

| Compliance burden | Concentrated at year-end | Distributed throughout the year |

Quarterly visibility enables better tax planning and cash flow management. When you know your projected tax liability in August rather than January, you can set aside funds gradually instead of facing a large unexpected bill. This foresight reduces financial stress and prevents the need for emergency borrowing to cover tax payments.

Digitisation also supports legitimate tax optimisation. Real-time visibility of your income and expenses helps you identify opportunities to claim all entitled reliefs and allowances. You might discover you are approaching a threshold that triggers additional obligations, enabling proactive planning to manage your tax position efficiently.

Whilst direct data on MTD for ITSA remains limited due to recent implementation, the existing MTD for VAT programme provides compelling evidence. Businesses using MTD for VAT report fewer errors, faster submissions, and improved financial awareness. These benefits translate directly to the income tax context, suggesting similar advantages for sole traders and landlords.

The wider economic impact matters too. A smaller tax gap means more funding for public services without increasing tax rates. Improved compliance creates a level playing field where all businesses contribute fairly. Digital systems reduce HMRC administrative costs, potentially enabling better taxpayer support and faster query resolution.

Simplify your MTD journey with VoxaMTD

Navigating MTD requirements need not overwhelm your business operations. VoxaMTD offers free MTD software for sole traders and landlords designed specifically for UK self-assessment taxpayers facing the new quarterly reporting obligations. The platform handles digital record-keeping, automatic expense categorisation, and direct HMRC submissions through an intuitive interface that requires no accounting expertise.

Whether you operate as a sole trader managing business income or a landlord tracking rental properties, VoxaMTD adapts to your specific situation. The software supports quarterly updates with built-in deadline reminders, ensuring you never miss a submission date. Integrated bank connections capture transactions automatically, whilst AI-powered categorisation reduces manual data entry to minutes per month. When tax year end arrives, the platform guides you through your final declaration, reconciling all quarterly updates into a complete annual picture. Start your free account today and transform MTD compliance from a burden into a streamlined routine.

Frequently asked questions

What exactly is Making Tax Digital for Income Tax Self Assessment?

Making Tax Digital for Income Tax Self Assessment is a HMRC programme requiring sole traders and landlords above income thresholds to maintain digital records and submit quarterly updates electronically. It replaces traditional paper-based annual tax returns with ongoing digital engagement throughout the tax year.

When does MTD for ITSA become mandatory for me?

Mandatory dates depend on your annual income threshold. If your business or property income exceeds £50,000, you must comply from April 2026. The threshold drops to £30,000 in April 2027 and £20,000 in April 2028, bringing more taxpayers into scope progressively.

What software do I need for MTD compliance?

You need HMRC-compatible software that maintains digital records and submits quarterly updates directly to HMRC systems. Options range from free platforms for basic compliance to paid solutions with advanced features, plus bridging software if you prefer spreadsheets.

What are the quarterly submission deadlines?

Quarterly updates are due one month after each quarter ends, with specific deadlines on 7 August, 7 November, 7 February, and 7 May. Your final declaration reconciling the full tax year remains due by 31 January following the tax year end.

What happens if I miss a quarterly deadline?

Missing a quarterly deadline triggers an initial penalty of £200. Continued non-compliance results in daily penalties of £10 starting 90 days after the deadline, potentially accumulating to thousands of pounds annually. Systematic compliance through reliable software prevents these costly consequences.

How does quarterly reporting benefit my business?

Quarterly reporting provides ongoing visibility of your tax position, enabling better cash flow planning and earlier error detection. You receive real-time tax estimates after each update, avoiding year-end surprises and allowing gradual tax payment provisioning throughout the year.