TL;DR:

- Making Tax Digital requires quarterly summaries of income and expenses, not instant transaction reporting.

- From April 2026, sole traders and landlords with income over £50,000 must comply, with thresholds rising later.

- Proper preparation and digital record-keeping can reduce errors, penalties, and improve financial planning.

Most sole traders and landlords hear 'real-time tax reporting' and picture a system where every sale, invoice, or rent payment pings HMRC the moment it happens. That picture is wrong, and the misunderstanding causes real anxiety ahead of the April 2026 Making Tax Digital (MTD) mandate. In practice, real-time reporting under MTD means sending quarterly summaries of your income and expenses through compatible software, giving HMRC closer-to-current visibility rather than a single annual snapshot. This guide explains exactly what that looks like, who it applies to, what gets submitted, and how to stay compliant without the stress.

Table of Contents

- What 'real-time' means under Making Tax Digital

- Who must report and what gets submitted?

- Exemptions, special rules, and penalties

- How does real-time reporting support better compliance?

- What most people misunderstand about 'real-time' tax reporting

- Next steps: get ready for digital tax reporting

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Quarterly summaries, not instant reporting | Real-time tax reporting for MTD means sending updates every quarter, not after each transaction. |

| Multiple income, multiple reports | Each business or property income must be reported separately, often requiring more than one quarterly update. |

| Easements and exemptions | Special rules help smaller businesses and some are exempt, but penalties apply if you delay from year two. |

| Improved financial visibility | Quarterly submissions give you and HMRC a clearer, up-to-date view of your taxable income for better planning. |

| Start with the right tools | Compliance requires compatible software or bridging solutions to keep digital records and submit updates. |

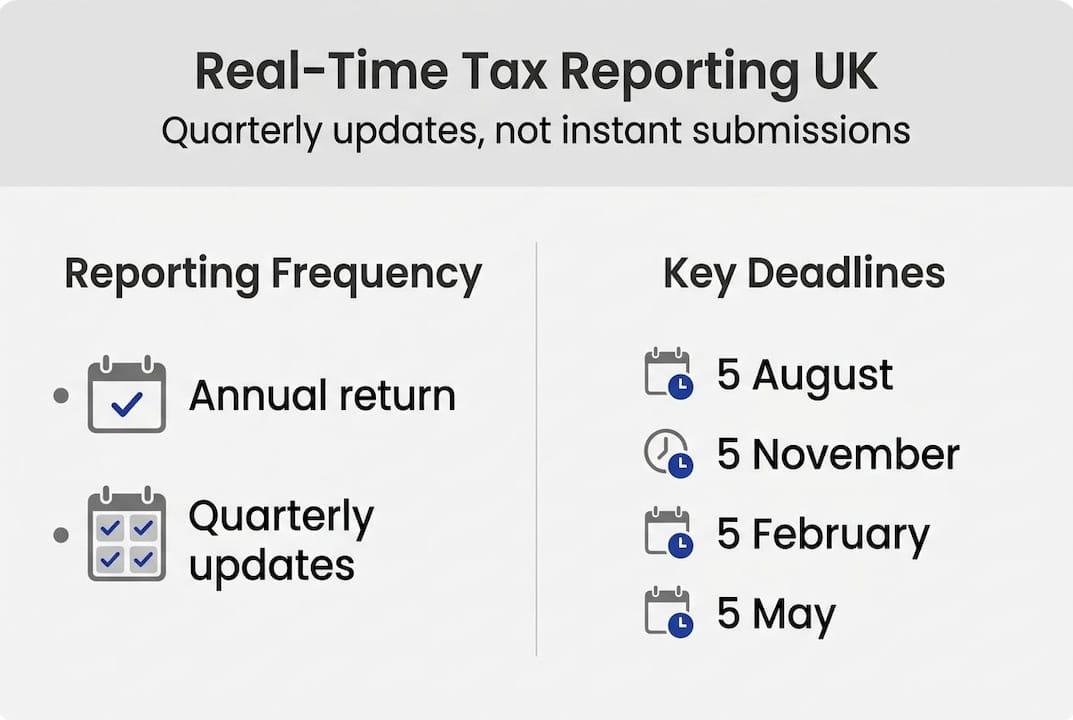

What 'real-time' means under Making Tax Digital

The phrase 'real-time' is borrowed from finance and technology, where it genuinely does mean instant. Under MTD for Income Tax, it means something more measured. You send HMRC a cumulative summary of your income and expenses four times a year, via MTD-compatible software, rather than waiting until the January self-assessment deadline to report everything at once.

Think of it like a quarterly health check rather than an annual medical. Each update does not trigger a tax payment or a full calculation. It simply keeps HMRC's picture of your finances more current throughout the year.

Each quarterly update typically includes:

- Total income received during the period

- Allowable expenses categorised by type

- Cumulative figures carried forward from earlier quarters

- Adjustments for any corrections to previous periods

The contrast with the old annual return is significant. Previously, you could ignore your records for eleven months and then scramble in January. Under MTD, you are expected to maintain digital records continuously and submit four times per year.

"Making Tax Digital requires businesses and landlords to keep digital records and send summary updates to HMRC each quarter using compatible software, providing closer to real-time visibility of tax affairs." — HMRC, How Making Tax Digital works

| Feature | Annual self-assessment | MTD quarterly updates |

|---|---|---|

| Frequency | Once per year | Four times per year |

| Records required | Paper or digital | Digital only |

| Tax payment triggered | Yes, January/July | No, estimates only |

| HMRC visibility | Delayed by up to 22 months | Within weeks of quarter end |

| Software required | Optional | Mandatory |

The quarterly deadline structure runs to fixed dates: 5 August, 5 November, 5 February, and 5 May. Miss one, and you accumulate a penalty point under the new system, which we will cover shortly.

Who must report and what gets submitted?

From April 2026, sole traders and UK landlords with qualifying income above £50,000 must comply. Those earning above £30,000 follow in April 2027. HMRC has confirmed further thresholds will be consulted on after that.

What counts as a separate income source matters enormously here. Separate quarterly updates are required per income source: each sole trade counts individually, all UK property income is treated as one source, and overseas property is reported separately. If you run two sole trades and rent out a property, you face three sets of quarterly obligations.

Here is a summary of how different income types are handled:

| Income source | Treated as | Updates per year |

|---|---|---|

| Single sole trade | One source | 4 |

| Two sole trades | Two sources | 8 |

| UK rental property | One source (all UK property combined) | 4 |

| Overseas rental property | Separate source | 4 |

| Employment income | Not in MTD scope | 0 |

For multi-source taxpayers, the process works as follows:

- Maintain separate digital records for each income source throughout the quarter.

- Reconcile each source at the quarter end before the submission deadline.

- Submit updates for each source individually through your MTD software.

- Review the cumulative tax estimate HMRC returns after each submission.

- Use that estimate to plan cashflow and set aside funds for your final bill.

Not every business faces the full burden. Easements apply for those below the VAT threshold, who can submit total income and expenses rather than line-by-line records. Joint property owners only need to report their income share. Retailers can use daily gross takings summaries rather than individual transaction records.

Pro Tip: If you manage multiple income sources, set up a separate folder or category within your MTD software for each one from day one. Mixing records mid-year creates reconciliation headaches that cost far more time than the initial setup.

You can cross-reference your specific obligations against an income tax checklist for sole traders or check the landlord MTD deadlines that apply to your situation.

Exemptions, special rules, and penalties

Not everyone falls under MTD for Income Tax. The following groups are currently exempt or excluded:

- Digitally excluded individuals: those who cannot use digital tools due to age, disability, or lack of internet access (you must apply to HMRC for this exemption)

- Partnerships: not yet mandated, though this is expected to change

- Estates and trusts: outside the current scope

- Non-UK residents: generally excluded from MTD ITSA

Applying for digital exclusion requires contacting HMRC directly and demonstrating why digital reporting is not reasonably practicable for you. It is not automatic.

The penalty regime is one of the most misunderstood parts of the new system. Points-based penalties apply from year two: each late quarterly submission earns one penalty point, and reaching four points triggers a £200 fine. Points reset only once you have submitted on time for a set period.

The good news for 2026/27 is a soft landing: HMRC will not issue penalties for late quarterly submissions in the first year. This is a genuine window to get your processes right. But it is not a reason to be complacent. The points clock starts ticking from year two, and four missed deadlines in a single year will cost you £200 immediately.

The UK tax gap stands at 5.3% (£46.8 billion) for 2023/24, with small businesses accounting for 60% of that figure. MTD is specifically designed to reduce careless errors, which make up 31% of the gap.

Pro Tip: Treat the soft landing year as a dress rehearsal, not a holiday. Use it to test your software, confirm your submission dates, and iron out any record-keeping gaps before real penalties apply.

For a full breakdown of what happens when you miss a deadline, the MTD penalty details are worth reviewing before April.

How does real-time reporting support better compliance?

Quarterly reporting is not just an administrative burden. It has measurable compliance benefits for both you and HMRC, and some practical financial advantages that are easy to overlook.

Because cumulative summaries flow via API from your MTD software to HMRC after each quarter, you receive an estimated tax liability in return. That estimate is not a bill. It is a planning tool. You can use it to set aside the right amount each quarter rather than facing a large, unexpected payment in January.

The compliance benefits are substantial:

- Fewer year-end errors: catching miscategorised expenses quarterly rather than annually reduces the risk of mistakes compounding

- Earlier visibility for HMRC: HMRC can identify anomalies sooner, reducing the likelihood of investigations based on sudden year-end discrepancies

- Better cashflow planning: knowing your estimated liability after each quarter lets you manage your money with more precision

- Reduced admin at year end: if records are maintained throughout the year, the final declaration becomes a review rather than a reconstruction

- Audit trail: digital records create a clear, timestamped history that is far easier to defend if HMRC ever queries your figures

The UK tax gap of £46.8 billion in 2023/24 is dominated by small business errors and omissions. MTD VAT, introduced in 2019, already yielded an estimated £185 to £195 million in additional revenue in its first year, not through new taxes, but through error reduction. MTD for Income Tax is projected to generate £1.95 billion in additional compliance by 2029/30.

Those numbers reflect a simple truth: when people maintain records regularly, they make fewer mistakes. The digitisation benefits are not theoretical. They show up in lower error rates and fewer penalty notices. Understanding the quarterly submission process in detail will help you see where your current record-keeping habits need adjusting.

What most people misunderstand about 'real-time' tax reporting

Here is the uncomfortable truth: the anxiety around real-time reporting is mostly self-inflicted, and it stems from a word that was always slightly misleading.

'Real-time' conjures images of constant monitoring, instant submissions, and HMRC watching every transaction. The reality is four updates per year, each one a summary. That is less frequent than most businesses already review their finances informally.

What we find, working with sole traders and landlords preparing for this change, is that the people most stressed are often those who have been doing the least record-keeping. For anyone already reconciling their accounts monthly, quarterly MTD submissions are genuinely straightforward. The mandate is not creating new work so much as formalising work that good businesses were already doing.

The easements are also chronically underused. Many landlords below the VAT threshold do not realise they can submit summary totals rather than itemised records. Bridging software makes compliance accessible even for those who prefer spreadsheets. These options exist and are legitimate.

The deeper point is this: quarterly check-ins build better financial habits. The businesses that will thrive under MTD are not the ones that treat it as box-ticking. They are the ones that use the MTD framework as a prompt to understand their own numbers more clearly, quarter by quarter.

Next steps: get ready for digital tax reporting

If this article has clarified what real-time reporting actually involves, the next step is making sure your setup is ready before April 2026.

VoxaMTD is a free, HMRC-recognised MTD platform built specifically for UK sole traders and landlords. It handles quarterly submissions directly to HMRC, imports bank transactions automatically, and includes an AI-powered receipt scanner to keep your records clean throughout the year. Landlords get a dedicated dashboard with a Section 24 calculator and capital allowances tracking. Sole traders get mileage logging, home office tools, and payments on account projections. You can check whether you need MTD using the free checker tool, explore the landlord-specific features, or review VoxaMTD pricing to find the tier that fits your situation.

Frequently asked questions

Is every transaction reported instantly with MTD for Income Tax?

No. MTD means quarterly summary updates, not live individual transaction reporting. You send a cumulative summary of income and expenses four times per year.

Do I have to use accounting software for MTD submissions?

Yes, HMRC-compatible software is mandatory, but spreadsheets with bridging software are a permitted route if you prefer to keep working in Excel or similar tools.

What happens if I miss a quarterly update deadline?

In 2026/27 there are no penalties due to the soft landing period, but from year two, each late submission earns a penalty point, with a £200 fine triggered at four points.

If my property income is below the VAT threshold, do I still send detailed updates?

No. Landlords below the VAT threshold can submit total income and expenses as a summary rather than itemised, line-by-line records.

Can someone submit my MTD updates for me?

Yes. An authorised agent or accountant can submit your quarterly MTD updates on your behalf, which is a practical option if you prefer professional oversight of your submissions.