TL;DR:

- Making Tax Digital for Income Tax Self Assessment changes record-keeping to quarterly summaries, not payment frequency.

- From April 2026, those earning over £50,000 must submit four digital income and expense summaries annually.

- Proper digital software and timely preparation are essential to stay compliant and avoid penalties.

Many sole traders and landlords hear "quarterly tax submissions" and immediately picture four tax bills landing on their doormat every year. That fear is understandable, but it is also completely wrong. Making Tax Digital (MTD) for Income Tax Self Assessment (ITSA) changes how you report to HMRC, not how often you pay. From April 2026, if your qualifying income exceeds £50,000, you will send digital summaries of your income and expenses four times a year. This guide walks you through exactly what that means, who is affected, when deadlines fall, and how to stay compliant without the stress.

Table of Contents

- What are quarterly tax submissions under Making Tax Digital?

- Who needs to submit quarterly returns and when?

- How to prepare and submit your digital updates

- Penalties, exemptions, and common mistakes

- An expert perspective on real-world MTD compliance

- Simplify your quarterly tax submissions with the right tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| No more frequent tax payments | Quarterly tax submissions do not change when you need to pay your tax bill. |

| Digital records are essential | Using MTD-compatible software for ongoing records is now mandatory for most over £50,000. |

| Deadlines matter | Filing on time prevents new penalties after the 2027/28 tax year. |

| Check for exemptions | Simplified rules or exemptions are available for lower incomes and digital exclusion. |

What are quarterly tax submissions under Making Tax Digital?

Let's clear up the biggest misconception first. Quarterly submissions under MTD are digital summaries of income and expenses sent to HMRC four times a year via compatible software, not full tax returns or payments. You are essentially telling HMRC what came in and what went out during each three-month period. Nothing more.

No extra tax bill arrives at the end of each quarter. Your Self Assessment payment deadline stays firmly on 31 January, just as it always has. What changes is the rhythm of your record-keeping, not your cash flow.

So why is HMRC doing this? The answer lies in reducing the enormous volume of errors that pile up when people scramble to recall twelve months of transactions in January. By spreading the admin across the year, HMRC expects fewer mistakes, fewer penalties, and better financial visibility for taxpayers. If you want a broader picture of how this fits into the wider shift, the UK tax digitisation guide covers the full context well.

Here is a quick comparison to make the difference crystal clear:

| Feature | Traditional Self Assessment | MTD quarterly updates |

|---|---|---|

| Frequency | Once per year | Four times per year |

| Content | Full tax return | Income and expense summary |

| Payment triggered? | Yes (31 Jan) | No |

| Software required? | No | Yes |

| Corrections allowed? | Via amendment | Via later updates or Final Declaration |

The digital tax return process still exists at year-end. You will still complete a Final Declaration (the MTD equivalent of your Self Assessment return) after the tax year closes. Quarterly updates feed into that, but they do not replace it.

"MTD quarterly updates are not tax returns and do not trigger payments. They are structured data summaries designed to keep your records current and accurate throughout the year." — official MTD quarterly update guidance

Who needs to submit quarterly returns and when?

Not everyone is affected immediately. MTD for ITSA rolls out in phases based on income thresholds, and the MTD rule changes are staggered deliberately to give people time to prepare.

Phase 1 begins on 6 April 2026 and applies to sole traders and landlords whose gross qualifying income (self-employment plus property combined) exceeds £50,000, based on the 2024/25 tax year figures. That affects 864,000 taxpayers in the first wave alone. The threshold then drops to £30,000 in April 2027, pulling in a further tranche of filers, and falls again to £20,000 in April 2028. At that point, roughly 2.9 million of the estimated 7 million ITSA filers will be within scope.

| Phase | Start date | Income threshold |

|---|---|---|

| Phase 1 | April 2026 | Over £50,000 |

| Phase 2 | April 2027 | Over £30,000 |

| Phase 3 | April 2028 | Over £20,000 |

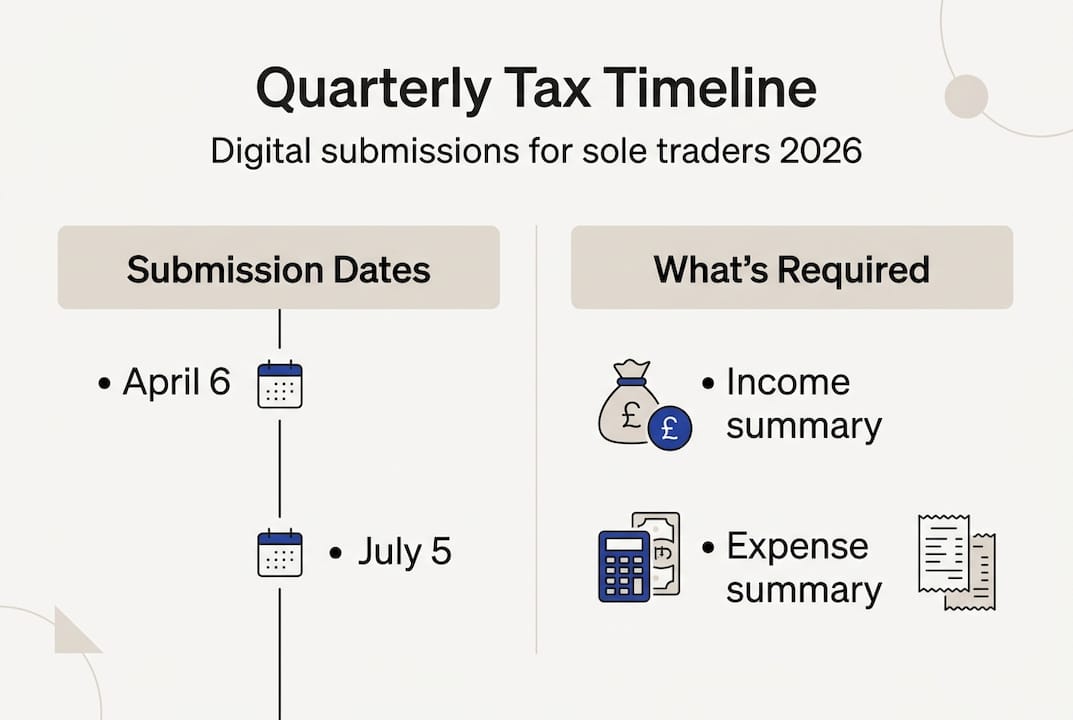

Deadlines follow a fixed pattern. Each quarter is cumulative and year-to-date, meaning each update builds on the previous one rather than starting fresh:

- Q1: 6 April to 5 July, due by 7 August

- Q2: 6 April to 5 October, due by 7 November

- Q3: 6 April to 5 January, due by 7 February

- Q4: 6 April to 5 April, due by 7 May

If you prefer calendar quarters (ending 31 March, 30 June, 30 September, 31 December), HMRC does permit an alternative quarterly period. This suits businesses whose accounting already runs on calendar months, and it can simplify bank reconciliation considerably.

Pro Tip: Check your 2024/25 tax return now. If your combined self-employment and property income exceeds £50,000, you are in scope from April 2026. Do not wait until the deadline is looming to set up your software. Good MTD bookkeeping for sole traders starts well before the first submission date.

Missing these digital tax deadlines carries real consequences, which we cover shortly. For now, the key point is that the clock starts ticking from 6 April 2026 for those above the £50,000 threshold.

How to prepare and submit your digital updates

Once you know you are in scope and when to file, the practical question becomes: how do you actually do it? The process is more straightforward than most people expect, provided you have the right setup from the start.

Every business within MTD must use MTD-compatible software to maintain digital records and submit updates. Spreadsheets alone do not qualify unless they are linked to bridging software that connects to HMRC's API. Here is how the process works step by step:

- Record transactions continuously. Every item of income and every expense must be logged in your software throughout the quarter. The more consistently you do this, the less work piles up at submission time.

- Categorise income and expenses. HMRC requires transactions to be grouped into specific categories (for example, cost of goods sold, travel, professional fees). Good software handles much of this automatically.

- Review the quarterly summary. Before submitting, check the figures your software has generated. Look for missing transactions, duplicate entries, or anything that looks out of place.

- Submit the update to HMRC. Your software sends the summary directly to HMRC via the API. You will receive a confirmation. The whole process takes minutes once records are in order.

- Correct errors later if needed. You do not need to upload receipts, and if you spot a mistake after submission, you can correct it in a subsequent quarterly update or in the Final Declaration at year-end.

For businesses with simpler finances (income below £90,000 per source), HMRC permits simplified three-line accounts: total income, total expenses, and net profit. This reduces the categorisation burden significantly. Joint landlords also benefit from specific easements, allowing a single entry per category rather than splitting every transaction.

Pro Tip: Set four calendar reminders now, one week before each submission deadline. Use that week to reconcile your bank statements, check for missed allowances such as mileage or home office costs, and review the summary before hitting submit. A few minutes of review can save hours of correction later. The quarterly reporting process tips article has more detail on building this habit.

Penalties, exemptions, and common mistakes

With your submissions in hand, do not overlook what happens if you miss a deadline or encounter a situation that falls outside the standard rules.

The good news for 2026/27 is that HMRC has confirmed a soft landing period. No penalty points will be issued for late quarterly updates during the first year. This gives newly mandated filers breathing room to get their systems in place without fear of immediate financial consequences.

From 2027/28, however, the points-based penalty system kicks in fully:

- 1 point for each late quarterly submission

- £200 fine when you reach 4 points (for quarterly filers)

- Points expire after a set period of good compliance

- Up to £3,000 for record-keeping failures

Exemptions do exist. You may qualify to be excluded from MTD if your income per source falls below the current threshold, or if you can demonstrate digital exclusion due to age, disability, or remote location. Joint property owners and those using simplified three-line accounts also benefit from specific easements.

Common mistakes to avoid:

- Missing submission deadlines because you forgot the quarterly rhythm

- Failing to keep digital records and trying to reconstruct transactions at quarter-end

- Assuming quarterly updates replace the Final Declaration (they do not)

- Using incompatible software that cannot connect directly to HMRC's API

Pro Tip: Even if you believe you are exempt, maintaining digital records voluntarily is worth considering. It makes your Final Declaration far simpler and gives you a clearer picture of your finances year-round. The digital submission guide for landlords covers landlord-specific exemptions in more detail.

An expert perspective on real-world MTD compliance

Here is something the official guidance rarely says plainly: quarterly updates will not feel burdensome if your bookkeeping is already tidy. The problem is that most sole traders and landlords do not have tidy bookkeeping. They have a shoebox of receipts and a vague memory of what happened in April.

MTD forces a habit change, and that is actually its most valuable feature. Real-time compliance reduces year-end errors, but the deeper benefit is that you stop being surprised by your own tax bill. When you review income and expenses every quarter, you can spot problems early, claim allowances you would otherwise forget, and plan your payments on account with confidence.

One subtlety worth understanding: quarterly updates exclude tax adjustments and allowances. Capital allowances, pension contributions, and loss relief are all handled in the Final Declaration. So the quarterly figure is not your taxable profit. It is a raw summary. Do not panic if it looks higher than expected.

If you run multiple businesses, each one needs a separate quarterly update, but HMRC issues only a single penalty point per period regardless of how many businesses you have. That is a small mercy. Over time, the digital tax trends for sole traders point firmly in one direction: those who adapt early will find compliance genuinely less stressful than the old January scramble.

Simplify your quarterly tax submissions with the right tools

If reading this has made you realise your current record-keeping setup is not MTD-ready, now is the right time to act. VoxaMTD is a free, HMRC-recognised platform built specifically for MTD software for sole traders and landlords, handling quarterly submissions directly to HMRC via the production API.

For free MTD software for landlords, VoxaMTD includes a dedicated dashboard with Section 24 mortgage interest calculations, automatic bank transaction imports, and AI-powered expense categorisation. Sole traders get mileage tracking, home office calculators, and payments on account projections. The VoxaMTD platform also features Alex AI Accountant, a voice-powered assistant available 24/7 to answer your tax questions conversationally. Getting set up before April 2026 means your first quarterly update will be a non-event rather than a last-minute scramble.

Frequently asked questions

Does a quarterly tax submission mean I pay tax more often?

No. Quarterly updates are summaries only, not payments. Your Self Assessment payment deadline remains 31 January each year, completely unchanged by MTD.

When do I need to file the first MTD quarterly update?

The first update covers 6 April to 5 July 2026 and must be submitted by 7 August 2026 for those in scope from April 2026.

What happens if I miss a quarterly submission deadline?

During 2026/27, HMRC's soft landing means no penalty points are issued for late updates. From 2027/28, the full points-based penalty system applies.

Are any sole traders or landlords exempt from quarterly submissions?

Yes. If your qualifying income is below the current threshold, or you qualify for digital exclusion, you may not need to file quarterly updates at this stage.

Recommended

- What is UK tax digitisation? A guide for sole traders

- Navigate digital tax trends: a 2026 guide for sole traders

- UK sole trader bookkeeping guide for Making Tax Digital 2026

- Understanding digital tax deadlines: 50,000+ UK traders affected

- Master the tax filing procedure for UK consultants 2026 - Price & Accountants

- Top Tax Questions Small Business Owners Ask in 2025 - Ready Accounting