Most sole traders and landlords assume HMRC will hand them software, walk them through bookkeeping, or somehow manage the digital side of things. That assumption is wrong, and it is costing people time. With over 864,000 individuals required to join Making Tax Digital from 6 April 2026, the gap between what people expect and what HMRC actually does has never mattered more. This article sets the record straight, explaining HMRC's precise responsibilities, what you must do yourself, and how to stay compliant without the stress.

Table of Contents

- What is Making Tax Digital and why does it matter?

- HMRC's core responsibilities in Making Tax Digital

- What compliance means for you: records, software, and updates

- Exemptions, deferrals, and edge cases: what if you cannot comply?

- Enforcement, penalties, and the 'soft landing' period

- The debate: benefits, criticisms, and HMRC's evolving strategy

- Navigate MTD with confidence: explore HMRC-compatible solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| HMRC sets the rules | HMRC mandates and enforces MTD but does not provide software or manage your records. |

| Digital compliance now required | Most sole traders and landlords above £50,000 income must use compatible software from April 2026, with lower thresholds soon after. |

| Quarterly submissions essential | Quarterly updates and final declarations become mandatory to avoid penalties. |

| Exemptions are available | Apply directly to HMRC if you face digital exclusion or qualify for automatic exemption. |

| Trusted software solutions help | Choosing an HMRC-recognised software eases compliance and reduces risk of fines. |

What is Making Tax Digital and why does it matter?

Making Tax Digital for Income Tax Self Assessment (MTD for ITSA) is HMRC's programme to modernise how self-employed people and landlords report their income. Instead of one annual tax return, you submit quarterly updates through MTD-compatible software, followed by a final declaration at year end. The goal, according to HMRC, is to reduce errors and make tax administration simpler across the board.

The scale of this change is significant. HMRC mandates that sole traders and landlords with qualifying income over £50,000 in the 2024/25 tax year must join from 6 April 2026. The threshold drops to £30,000 in April 2027 and £20,000 in April 2028. In total, around 2.9 million people will be phased into the system by 2028. Understanding the impact of digital tax deadlines is essential if you want to avoid penalties.

Here is what MTD for ITSA covers:

- Who it applies to: Sole traders and landlords with qualifying gross income above the relevant threshold

- What changes: Quarterly digital updates replace the single annual return for income reporting

- What stays the same: A final declaration (similar to a self-assessment return) is still required each year

- When it starts: 6 April 2026 for those earning over £50,000

- What you need: HMRC-recognised software, not a spreadsheet or paper records

'Only 10% have signed up voluntarily as of March 2026, suggesting the majority of affected sole traders and landlords are yet to act.'

That figure is striking. It points to widespread confusion, not just about deadlines, but about what the whole system actually requires of you. The UK tax digitisation guide is a useful starting point if you want the full picture.

HMRC's core responsibilities in Making Tax Digital

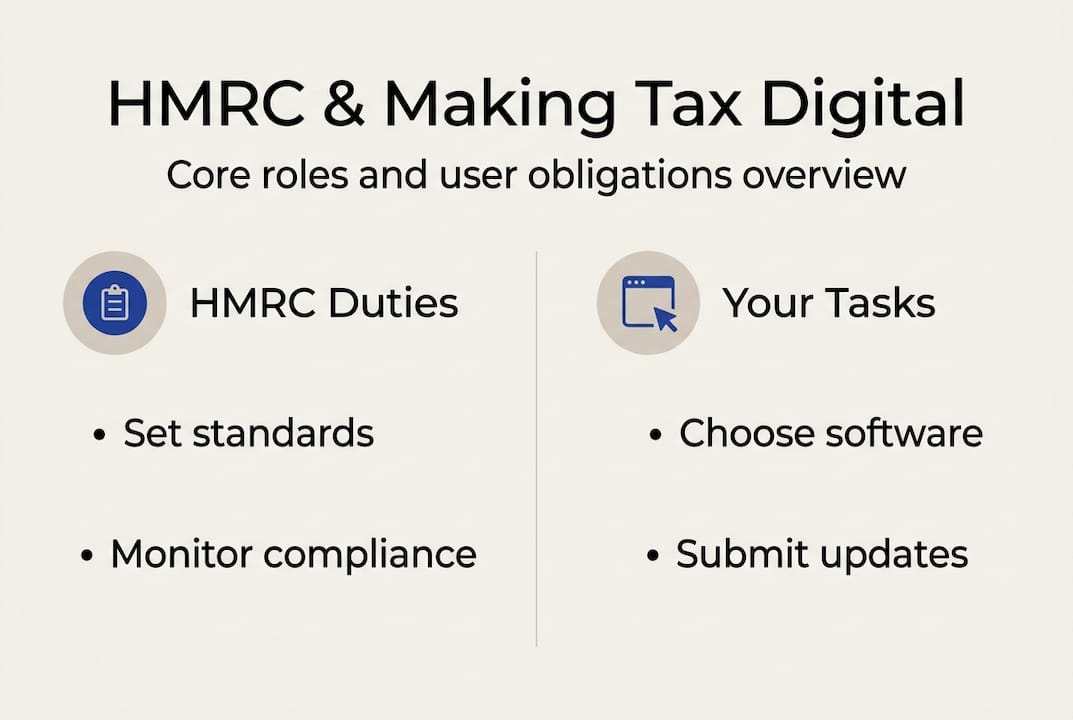

HMRC's role in MTD is often misunderstood. People expect a government-run portal, a free tool, or at least some form of direct assistance with their records. What HMRC actually does is quite different.

According to ICAEW's MTD overview, HMRC's role centres on enforcement, guidance, and system integration via APIs. It sets the rules, publishes the timelines, runs support webinars, and maintains the technical specifications that software providers must meet. It does not touch your records, enter your data, or provide the software you use to submit.

HMRC's responsibilities, in plain terms:

- Enforcement: Determines who must join MTD and when, and applies penalties for non-compliance

- Guidance: Publishes step-by-step processes for sign-up, software selection, and agent authorisation

- API integration: Maintains the technical infrastructure that allows compatible software to connect to HMRC systems

- Agent authorisation: Sets up the framework for accountants and tax agents to act on your behalf

- What HMRC does NOT do: Provide software, manage your records, categorise your expenses, or remind you of quarterly deadlines

Pro Tip: HMRC publishes a list of MTD population statistics and compatible software providers, but choosing the right tool is entirely your responsibility. Check the HMRC-recognised list before committing to any platform.

Understanding MTD regulations and landlord MTD deadlines will help you map out exactly what you need to do and when.

What compliance means for you: records, software, and updates

Compliance is not passive. You cannot wait for HMRC to prompt you or assume your accountant will handle everything without your involvement. Each income source, whether that is a sole trader business or a rental property, requires its own set of separate digital records and quarterly updates submitted through compatible software.

| Income threshold | Mandatory from | Estimated individuals affected |

|---|---|---|

| Over £50,000 | 6 April 2026 | ~864,000 |

| Over £30,000 | 6 April 2027 | Additional wave |

| Over £20,000 | 6 April 2028 | ~2.9 million total |

Here is how to get started with MTD compliance:

- Register for MTD for ITSA through your Government Gateway account before your mandatory start date

- Select HMRC-recognised software that suits your business type, whether you are a sole trader, landlord, or both

- Keep digital records of all income and expenses from the start of your first MTD period

- Schedule quarterly updates for the four reporting periods each tax year and submit them on time

- Use an agent if needed, but remember that you must authorise them explicitly before they can act on your behalf

One important point that catches many people out: quarterly updates are summaries, not full tax returns. They give HMRC a running picture of your income and expenses, but they do not replace the final declaration.

'Quarterly updates are summaries, not a replacement for a full annual return. In your first year, you must still file your self-assessment return as usual alongside your MTD obligations.'

The sole trader MTD bookkeeping guide and the landlord MTD submission guide both offer practical walkthroughs for each step. Reviewing MTD and penalties guidance is also worth doing before your first submission.

Exemptions, deferrals, and edge cases: what if you cannot comply?

Not everyone will be required to join MTD, and it is worth knowing whether you fall into an exempt category before you invest time and money in compliance.

Digital exclusion is the most common route to exemption. If age, disability, location (such as poor broadband access), or religious beliefs make digital record-keeping genuinely impractical, you can apply to HMRC for an exemption. You will need to provide supporting evidence, and HMRC will assess your case individually.

Some groups are automatically excluded, at least for now:

- Trustees and executors managing estates or trusts

- Lloyd's underwriters operating under specific arrangements

- Ministers of religion (excluded until 2029)

- Partnerships (rules are still being finalised)

- Individuals without a National Insurance number

- Non-residents subject to specific rules

Pro Tip: If you think you qualify for an exemption, apply to HMRC in writing with clear supporting evidence. Keep a copy of any written confirmation you receive. Do not assume exemption applies without going through the formal process.

For further clarity on terminology and categories, the MTD terms explained resource covers the key definitions in plain language.

Enforcement, penalties, and the 'soft landing' period

HMRC has introduced a points-based penalty system for MTD, and it works differently from the old fixed-fine approach. Miss a quarterly update and you receive one penalty point. Accumulate four points and you are charged a £200 penalty. Points reset after a sustained period of compliance.

| Penalty type | Trigger | Amount |

|---|---|---|

| Late submission (quarterly) | 1 point per missed update | £200 at 4-point threshold |

| Late submission (final declaration) | 1 point per missed filing | £200 at threshold |

| Late payment (15 days) | Unpaid tax after 15 days | 3% of outstanding amount |

| Late payment (30 days) | Unpaid tax after 30 days | Additional 4% interest |

The good news is that HMRC has confirmed a soft landing for 2026/27. During this first year, no penalty points will be issued for late quarterly updates. This gives you breathing room to get your systems in order, but it is not an excuse to delay. Payment penalties and interest still apply from day one.

The Deloitte MTD penalty overview provides a detailed breakdown of how the system works in practice. And if you want to stay on top of your MTD submissions, building a quarterly calendar now is the simplest way to avoid points altogether.

The debate: benefits, criticisms, and HMRC's evolving strategy

MTD is not without controversy. HMRC promotes it as a way to reduce errors, improve real-time visibility over tax liabilities, and make planning easier for self-employed people. In theory, knowing your approximate tax bill throughout the year rather than discovering it in January is genuinely useful.

But critics, including many accountants and small business groups, argue that MTD adds compliance burden and software costs without delivering meaningful benefits to taxpayers. The ICAEW's MTD overview reflects this tension, noting that the system is designed primarily to close the tax gap rather than simplify life for the self-employed.

Here is a balanced view from both sides:

- Benefits: Real-time tax estimates, reduced year-end scramble, fewer errors from digital records, better financial visibility

- Drawbacks: Additional software costs, time spent on quarterly submissions, learning curve for less tech-savvy users, complexity for those with multiple income sources

'Less than 10% signed up for MTD before the mandatory phase-in, hinting at hesitance among sole traders and landlords about the system's complexity and value.'

That low voluntary uptake tells its own story. Whether you see MTD as a burden or an opportunity, the mandate is real. The UK tax digitisation landscape is shifting, and the most practical response is to get ahead of it rather than wait.

Navigate MTD with confidence: explore HMRC-compatible solutions

Choosing the right software is the single most important decision you will make in your MTD journey. HMRC will not make it for you, and the wrong choice can mean missed deadlines, incompatible records, or unnecessary costs.

VoxaMTD is a free, HMRC-recognised platform built specifically for sole traders and landlords navigating MTD. It handles quarterly submissions directly to HMRC via production API, imports bank transactions automatically through open banking, and uses AI to categorise expenses and scan receipts. Landlords get a dedicated dashboard with a Section 24 calculator and capital allowances tracking. Sole traders get mileage tracking, home office calculators, and payments on account projections. If you want human support, the Professional tier connects you with a real accountant for quarterly reviews. Getting set up takes minutes, and the free tier covers everything you need to stay compliant from day one.

Frequently asked questions

Does HMRC provide software for Making Tax Digital?

No, HMRC does not provide tax software for MTD. You must select and pay for a compatible platform from an approved provider yourself.

What happens if I miss a quarterly update?

You receive one penalty point per missed update, and four points triggers a £200 charge. During the 2026/27 soft landing period, quarterly points are waived, but payment penalties still apply.

Who is exempt from Making Tax Digital requirements?

Those digitally excluded by age, disability, location, or religion can apply for exemption directly to HMRC. Trustees, executors, ministers of religion, and certain others are automatically excluded.

Do agents or accountants handle MTD requirements for me?

Agents can manage your MTD submissions with your explicit authorisation, but you remain responsible for choosing your software and approving their actions on your behalf.